Imperial Brands: Solemn

“We’ve announced a 4% increase in our ordinary dividend, and we’re on track with our GBP 1.45 billion share buyback. Now this is our fourth consecutive year of share buybacks and brings the total capital returned to investors since the program started to GBP 4.8 billion. Taken alongside dividend payments, total cumulative capital returns from FY‘21 to half year ‘26 now sit at GBP 11.5 billion. This represents around 77% of our market capitalization at the time of our Capital Markets Day back in January 2021.” - Murray McGowan, CFO, Imperial Brands, H1’26 remarks

The odds of any surprises in Imperial’s H1’26 results were low, as the company’s Trading Update was released just a month prior and its distribution arm, Logista, already reported its H1’26 results. The report once again affirmed the year’s trajectory. Met with a doubtful tone during the Q&A, that confidence was reiterated, yet again. The required delivery in H2 to meet the expressed targets is higher than in past years, but that is due to several notable one-offs recognized in the first half. The underlying strategy remains sensible and differentiated, communicated candidly and concisely. Driving all decisions is a solemn vow to deliver for shareholders.

Imperial Brands continues to carefully grow its NGP business, albeit at a much slower pace than others. Pulze has caught modest traction in select markets, while modern oral continues its laudable ascent. Skruf has become a leader in Norway. Zone has launched in the UK while it continues to grow volumes in the U.S., though heavier promotion has played a hand.

Regarding the U.S., considerable uncertainty has been introduced by the FDA’s new Guidance for Industry, which opens the doors for many competing products. Subsequent launches will drive next-gen category volumes. However, given heavy promotions, the value generated in the near term may be questioned. Imperial has a few cards up its sleeve in this regard, but will play them cautiously. In light of the FDA’s announcement, the company has chosen to sunset its vapor product in the U.S. market. While others may see this as yet another mistake in the NGP realm, I applaud the discipline to know when to fold ‘em. Lukas Paravicini again reminded listeners of the group’s conservative approach when it comes to new, less defined categories and markets:

As much as I understand the excitement in many markets about pouches, when you look at data, and remember, we are a consumer first and data-driven company, the data is showing that the markets are very small. And hence, as the fourth largest in the industry and a responsible player also in regards to our shareholders, we will double down on those markets where we have a business or where the market has been created, and we have a route to market.

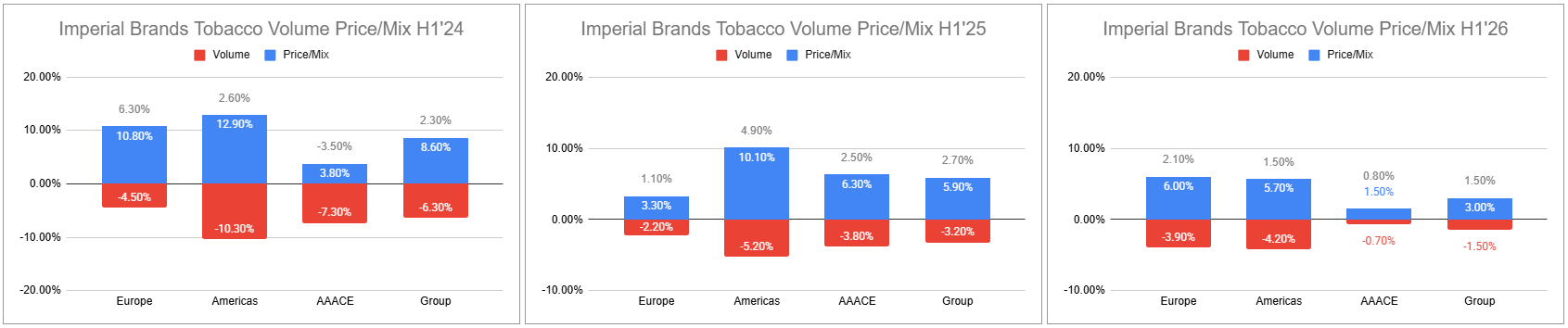

Although the NGP story continues to be the focus for many, Imperial’s is very much one predicated on the belief that cigarettes may linger far longer than most expect. On that front, there has been concern about market share losses in key countries.

I’ve often reiterated the dangers of focusing on market share. While Imperial itself has stressed its market share performance over the last several years, Paravicini delivered perhaps the most concise and honest views on the dynamics at hand:

Our share discussion and your focus on segment is really an evolution. I just want to reiterate how important share is for any company. But share is one of the metrics we look at next to net revenue, operating profit and many other metrics we have. And it’s really about this careful triangulation of price, volume and share in an environment where your gross margin has evolved significantly from the top to the bottom. We will play in all segments because we start with the consumer. Wherever the consumer is, we will be there. But while we double down on the top, we’ll also make sure that we are pricing responsibly at the bottom.

Supporting this notion are figures from the company showing wide gross margin disparities between products at the high and low ends of price within any given market, including a 2.5x differential in Spain, a 3x differential in Germany, and a staggering 7x differential in the United States. Volumes, often treated as equal, are nothing but. Tobacco profit was a bit soft in H1; however, the power of pricing and mix benefits supports a stronger second half of the year, and since there is increasing uncertainty facing NGP categories, there is comfort provided in Imperial’s preoccupation, which will likely prove more rigid.

Keep reading with a 7-day free trial

Subscribe to Invariant to keep reading this post and get 7 days of free access to the full post archives.