Intercontinental Exchange: The Green Light

“If you look around the table and you can’t tell who the sucker is, it’s you.” - Quiz Show

There’s a large amount of truth in that opening quote. But in finance, similar notions have been hyperbolized, making you think that every deal is full of sharks out for blood. The reality is, to get deals done, there are plenty of times when both parties walk away thinking they got a good deal but still left a bit on the table. In rarer instances, it can paradoxically appear that everyone is pulling the longer end of the stick.

Intercontinental Exchange acquiring Black Knight is one of those deals.

When announced in May of last year, there was immediate skepticism the deal would go through. The initial terms presented the cash and stock transaction valuing Black Knight at $85/share, with a total value of $13.1 billion. With the transaction price far above where shares traded to, it placed the odds of a successful close at basically a coin flip. Yet, on Friday, ICE and BKI announced entry into Agreement Containing Consent Orders (ACCO) with FTC’s Bureau of Competition. A successful close is slated for September 5th, 2023, with the terms of the deal modified distinctly:

To satisfy the FTC, the agreement is permitted to move forward 10 days post entry into the ACCO, with the previously announced divestitures of BKI’s Optimal Blue and Empower, to be completed within 20 days thereafter.

The amended Plan of Merger, as of March 7th, 2023, altered the full consideration to be received by Black Knight shareholders ($11.7 billion), with shareholders having a deadline of September 1, 2023 to elect the form of consideration they wish the receive: “equal to the sum, rounded to the nearest one tenth of a cent, of (x) $68.00 plus (y) the product, rounded to the nearest one tenth of a cent, of 0.0682 multiplied by the average of the volume weighted averages of the trading prices of ICE common stock on the New York Stock Exchange on each of the ten consecutive trading days ending on (and including) the trading day that is three trading days prior to the date on which the effective time of the acquisition occurs (the “Closing 10-Day Average ICE VWAP”); or a number of validly issued, fully paid and nonassessable shares of ICE common stock (the “Per Share Stock Consideration”) as is equal to the quotient, rounded to the nearest one ten thousandth, of (x) the Per Share Cash Consideration divided by (y) the Closing 10-Day Average ICE VWAP”

BKI shareholders are set to receive substantial compensation—a clear win. The purchaser of Optimal Blue and Empower, Constellation Software (TSE:CSU), is another beneficiary. The closing of the ICE + BKI deal is contingent on these divestments, making BKI and forced seller and allowing CSU to pick up these assets for attractive prices. While I don’t follow CSU closely, there has been continual skepticism that the company will continually be able to redeploy meaningful capital into acquisitions as it grows ever larger. These two deals, totaling over $1 billion, not only partly quash that skepticism but stand to make Constellation one of the largest participants in the mortgage origination software business in the United States.

As for ICE, the company avoids the lofty $725 million termination fee payable to BKI had the merger agreement been terminated. Without question, the loss of Empower and Optimal Blue mutes the dominant position the company would have found itself in. However, ICE is still in exceptional standing. To weigh the considerations, it’s worth revisiting some of the key points of the deal as well as ICE’s Mortgage Technology segment’s nascent history.

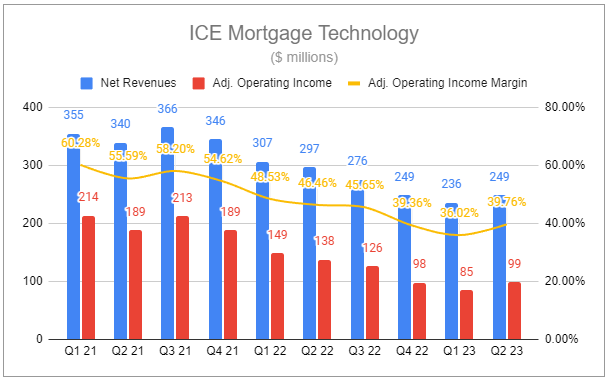

ICE’s Mortgage Technology segment was built upon it taking a majority interest in MERS in 2016, followed by acquiring the remainder in 2018, Simplifile in 2019, and Ellie Mae in 2020. The rationale? The U.S. mortgage industry is woefully inefficient and is still caught up using a variety of analog processes. By building out digital solutions, ICE would be able to provide better outcomes while capturing total value share. Pro forma year to date, since 2018, ICE has grown segment transaction revenues at a mere 1% CAGR. However, segment recurring revenues have grown at a CAGR of 14%. Weakness in the mortgage market is unmissable in transaction revenues over the last several years:

Settings aside ~$200 million in cost synergies from the BKI deal, ICE stands to benefit in a number of ways. BKI’s revenues are far less weighted to transactions and are largely related to data & analytics and servicing software. In agreement with Constellation, Optimal Blue will also be fully available to ICE customers on its open network. Further, there is still the potential for ICE to internally develop or acquire additional components to move closer to its goal of creating the first end-to-end mortgage software. Building out such an offering will allow greater conversion, retention, and ultimately pricing power—driven by the ability to further speed up mortgage processes, reduce error rates, and minimize other associated costs. Even without the deal closing, continued successes highlight ICE’s winning approach, as captured in comments made by Warren Gardiner, ICE CFO, during the Q2 2023 call (emphasis added):

Importantly, the vast majority of these customers not only remain on the Encompass and ICE Mortgage Technology platform, but have also signed multiyear contract renewals. While macro conditions appear to be stabilizing and year-over-year pressure on forward-looking application volumes appears to be moderating, evidenced by a mid-teen decline in July applications compared to a nearly 30% decline in 2Q and a nearly 50% decline in the first quarter, current cyclical pressures are now likely to drive our recurring revenue growth into the low single-digit range for the full year. However, these same cyclical conditions and the need to reexamine legacy cost structures continues to attract customers that have not traditionally utilized the ICE Mortgage Technology platform. As an example, the top-5 bank that elected to replace their in-house solution with Encompass as their system of record for the retail channel last quarter has now also signed on as an Encompass customer for their correspondent channel.

In addition, CrossCountry Mortgage, a top 15 lender and Encompass user, signed on to utilize our analyzers in what was one of the largest data and analytics deals in our history, following JPMorgan's adoption of our analyzer suite last year. While these wins will take time to implement and are therefore not expected to impact our 2023 recurring revenues, it's a clear example of the increasing need for workflow efficiencies. And we expect there to be continued momentum through the balance of this year and into 2024.

Further context was provided during the Q&A of the call by Benjamin Jackson, ICE President (emphasis added):

We've had the Ellie Mae business now for 3 years, and we started talking about this just a couple of years ago. Most customers are on agreements that are around 4 to 5 years in duration. So we're roughly halfway through that transition. In terms of how the business is doing from a longer-term perspective, we feel great as we've been talking about on many of these calls how we've been repositioning the ICE Mortgage Technology company to really unlock long-term growth potential. And underneath the covers, we've seen a lot of success towards that.

The evidence to that effect is that over the last several quarters, we've mentioned that we've had success renewing more than 60% of our customers at higher subscriptions. And even when we do see that 40% or so or less that are renewing at lower subscription fees, the trade-off there is that we're getting a higher per closed loan fee on each of those. So when the market normalizes, that will be a tailwind towards our transaction revenues.

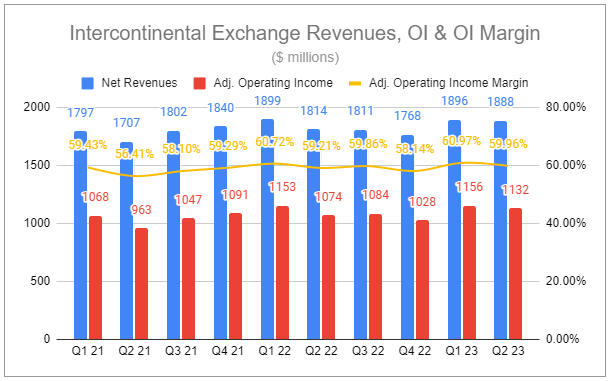

While we move closer to the deal closing, it’s worth noting that ICE’s other operating segments have been continuing to execute wonderfully. In Exchange, Energy has been especially impressive and continues to grow, with meaningful volume, open interest, and total share, with price increases on a variety of contracts in Q1 being carried forward nicely.

Growth in Fixed Income & Data Services continues to benefit from changes in interest rates, movements across bonds and treasuries, growth of passive investing, reliance on mission-critical data sets, and automation and efficiency initiatives.

Even with the massive drop in Mortgage Technology transactional revenue, the company as a whole is far from being in shambles.

At a 4% FCF yield on paper, ICE may not appear to be the most enticing name, though adjusting that figure for the impact of BKI points to something more alluring. It’s worth stepping back from the quarter-to-quarter noise and gyrations and articulating what this company represents:

Diverse operations across three operating segments that are all entrenched and benefiting from numerous long-term trends and tailwinds; becoming more important as the world becomes more complex.

Continued prioritization and shift from transactional and cyclical revenues to stable recurring revenues.

Incremental buildout of value-added offerings across all segments, providing long-term pricing power.

Absurdly high-margin activities that ultimately convert heavily to free cash flow.

This is a machine set to slowly return capital to shareholders while continuing to acquire and build quality assets. Last October, I wrote:

The company pushed hard into energy markets after the fall of Enron.

It charged into credit default swaps during the 2008 financial crisis.

And now, ICE is stepping on the accelerator in the mortgage ecosystem as rates continue to rise and real estate prices waver.

There continues to be limited enthusiasm for the current deal to close. Undoubtedly, the world is fixated on the short-term and not the full future cycles. That is likely to change the next time mortgages heat up. And when the next market crisis hits? You can expect Jeffrey Sprecher and ICE to be looking for targets.

If you enjoyed reading, hit “♡ like” and share this piece with someone.

Ownership Disclaimer

At the time of publishing this piece, I own positions in Intercontinental Exchange.

Disclaimer

This publication’s content is for entertainment and educational purposes only. I am not a licensed investment professional. Nothing produced under the Invariant brand should be thought of as investment advice. Do your own research. All content is subject to interpretation.

Tags: ICE 0.00%↑ BKI 0.00%↑ CSU 0.00%↑

I got involved post the sell off after the acquisition was announced. I hear pushback from others on the buyside about the lack of organic drivers, difficulty in pinning accretion, optically expensive prices paid, and concerns about growth rates.

If you step back from that I agree that this is a clearly advantaged business with long term tailwinds. Moreover, Jeff has knack for pulling really attractive economics out of hat and has turned around deals that were heading south. For me, this is a business that as you look farther and farther out the potential IRR spreads between a base and upside scenario become increasingly attractive with comparatively little impairment risk.

Looking forward to hearing what you have to say on this one in a few years.

Stellar work.