Altria: Lean

“We continue to press for actions that will shape a fully regulated industry and provide expanded product choices for adult nicotine consumers. And we returned significant value to our loyal shareholders during the first half of the year with more than $4 billion delivered through dividends and share repurchases. Our operating companies delivered strong financial results in a dynamic marketplace, allowing us to raise the lower end of our 2025 guidance range.” - William Gifford, Altria CEO, Q2’25 remarks

There remains a narrative that Altria is far behind in next-gen nicotine delivery, and thus must fully lean into a strategy wholly oriented to new products. But such a perspective fails to appreciate the value drivers of its legacy product portfolio, and revamping its stance risks eroding the parts of the business the company already excels in. This is not to say that the company should not or will not pursue new avenues. It has and continues to. Instead, it ought to keep lean on the cost side, and devote itself to ensuring its sharecount becomes ever leaner too.

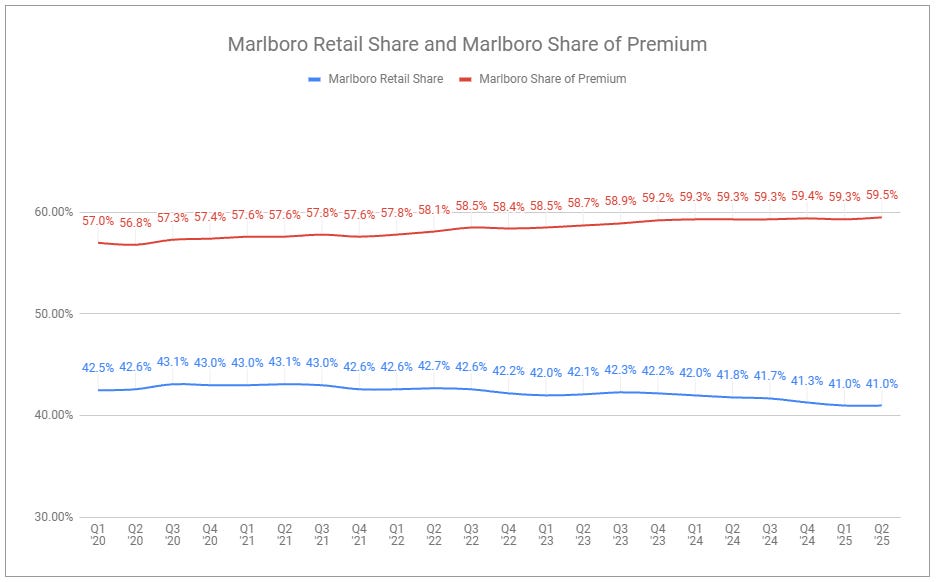

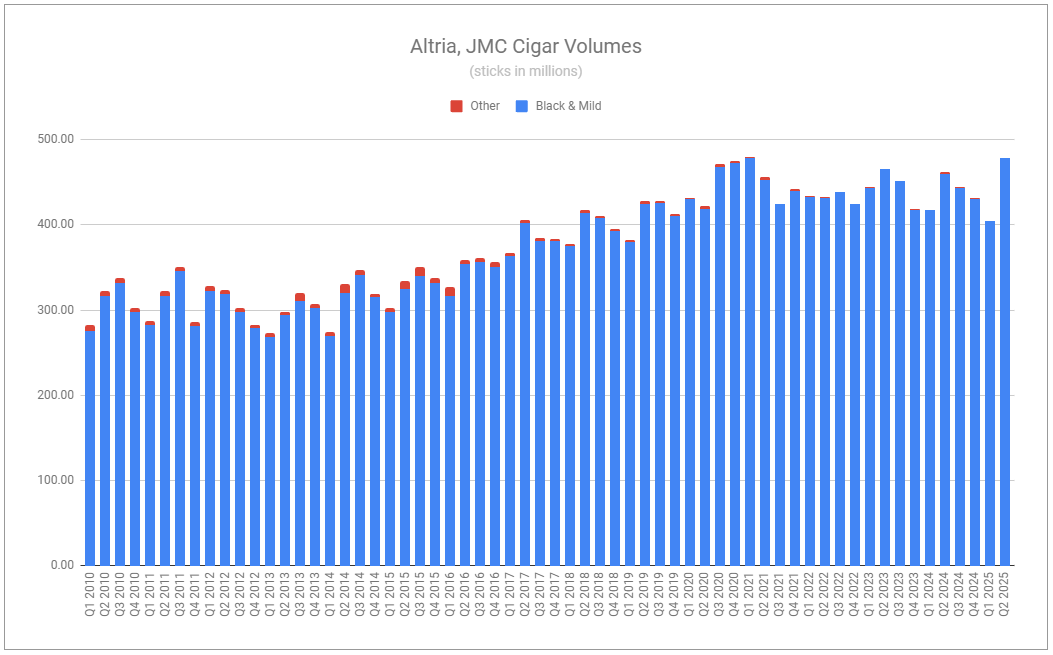

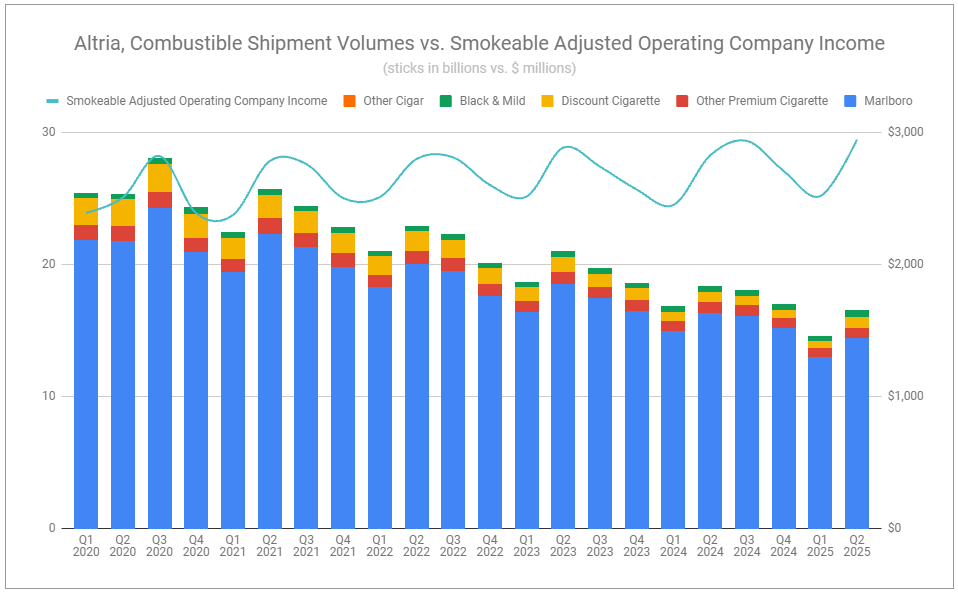

Altria’s Q2’25 results reiterated Marlboro’s dominant position and the fact that, truly, there aren’t many John Middletons. Volumes of the latter climbed 3.7% in Q2’25 and 0.6% for the first half of the year, while the former traded broad share for an incremental gain in the premium subsegment. While aggregate combustible volumes continued their elevated decline, it did not stop the segment from posting relatively robust operating profit growth of 3.5% for H1’25 through strong pricing.

The only factor seemingly out of place within Altria’s combustibles reporting is the expansion of Basic, a discount cigarette brand. On one hand, management highlighted that Basic’s market share gain had little impact on Marlboro—which should be expected as they compete on opposite sides of the price spectrum. However, to take resources to expand the footprint of a discount offering is incongruent with the strategy employed over the last handful of years, in which the company would maximize dollars, not share, as stressed by Altria’s CEO William Gifford during the group’s 2023 Investor Day:

We also observed certain branded discount offerings priced at deep discount levels. As we've noted in the past, some smokers will adjust their purchase behaviors based on short-term economic conditions. However, over the long term, we believe the majority of smokers continue to value the premium quality and consistency of brands like Marlboro. We remain premium focused to maximize long-term profit over low-margin share gains.

Over the previous several years, the company has appeared content to see the discount portion of its business erode. This latest action implies that the group expects pressures against U.S. consumers, expressed via downtrading, to persist for an extended period.

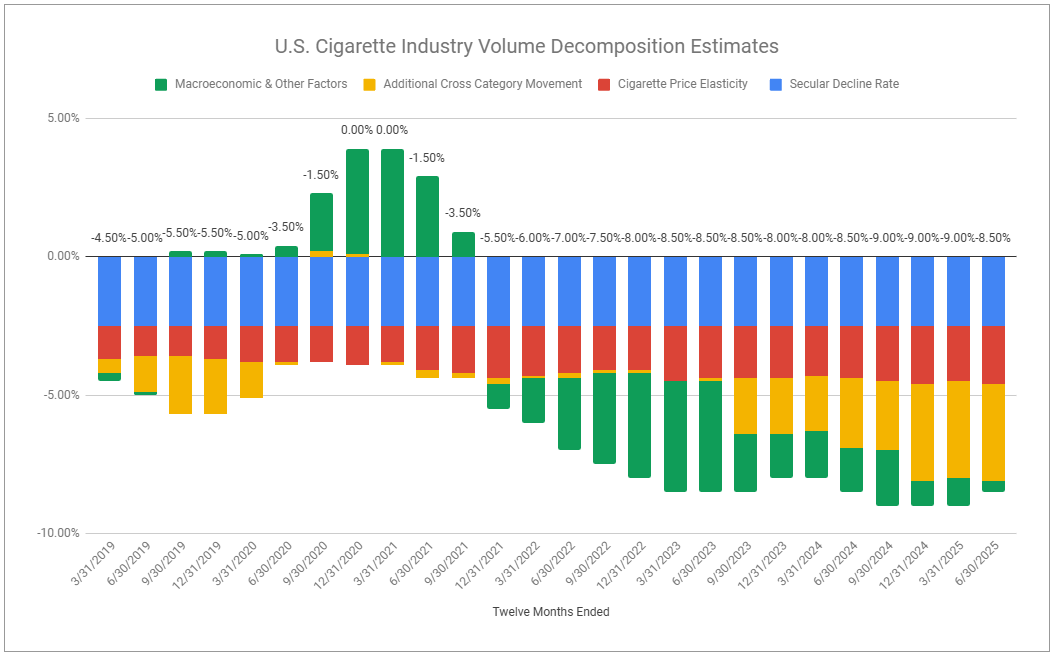

As the decline rate remains elevated, the factors shaping the decline of U.S. cigarette volumes continue to be a focus. Although the estimated decline rate declined sequentially, I remain unconvinced that such an occurrence marks a new trend. Altria highlighted U.S. consumers remaining under pressure, although, in their estimates, Macroeconomic & Other factors are suggested to have decreased marginally. At the same time, Cross-Category Movement, at the mid-point of the estimated range, persists at 3.5%.

At face value, the elevated rate of Cross-Category Movement may come as a surprise, as numerous layers of federal and state-level enforcement actions have been taken against illicit vapor. But there are two points to consider. First is that the resulting shortages of several leading illicit disposable vaping devices would not be fully reflected in Q2’25, due to the timing of the enforcement actions. This may provide some incremental benefit over combustibles over the next few quarters. More importantly, when looking long-term, I believe Cross-Category Movement into nicotine pouches will become an incrementally larger part of the CCM mix in the coming years.

Keep reading with a 7-day free trial

Subscribe to Invariant to keep reading this post and get 7 days of free access to the full post archives.