Listerine Royalties: The Origin Story and Valuation of a Uniquely Enduring Asset

“If a man can make me laugh and stimulate me intellectually, then I wouldn't mind if he was 4 ft. 8 in. with a huge belly. The only thing that would put me off is bad breath - but even that can be fixed. A bad personality isn't so easy to fix.” - Olga Kurylenko

What if there was a tariff on bad breath—a surcharge on oral health only escapable by those unconcerned with pesky things like personal hygiene?

Well, there’s already a tax. And you can own the rights to a piece of the proceeds.

Listerine Lore

In the nineteenth century, Louis Pasteur’s groundbreaking research formed our foundational understanding of the causation and prevention of disease. This subsequently influenced British surgeon Joseph Lister’s experimentations concerning wound infection, leading him to become known as the “father of modern surgery.” Several years later, understanding the critical importance of sterilization, the American Dr. Joseph Lawrence developed an alcohol-based concoction to be used as a germicide and surgical antiseptic. Honoring Dr. Lister, he dubbed it “Listerine.”

In 1881, aiming to boost the adoption of Listerine, Dr. Lawrence licensed his secret formula to a pharmacist by the name of Jordan Lambert. Then, in 1895, after varying degrees of advertising success, Listerine’s marketing focus pivoted toward dentists for oral care. By 1915, you could find Listerine in households all around the United States.

The original licensing contract signed between Dr. Lawrence and Jordan Lambert was a mere two sentences, with clear terms. Lambert’s company would be the sole producer and distributor of Listerine. And in the future, Dr. Lawrence would receive $20 for every gross (144 bottles) sold. This was later amended to be based on ounces sold to equivalize different container sizes.

But “the future,” as you may know, is a rather long time. In 1955, Jordan Lambert’s Lambert Pharmaceutical merged with Warner-Hudnut, and the new outfit, Warner-Lambert Pharmaceutical Company, contested the royalty agreement in federal court. Their main arguments were straightforward: Firstly, “the future” isn’t forever. Secondarily, the royalty agreement concerned Dr. Lawrence’s original formula—a trade secret that had been inadvertently published in 1931. They posited that since the trade secret was made public record, it wasn’t, by definition, secret, and therefore the agreement was no longer valuable or valid.

The court found the arguments dubious and upheld the original agreement, stating:

The plaintiff seems to feel that the 1881 and 1885 agreements are indefinite and unclear, at least as to the length of time during which they would continue in effect. I do not find them to be so. These agreements seem to me to be plain and unambiguous.

There is no ambiguity or uncertainty in this language. Nor can I ascertain any alternative or hidden meanings lurking within it.

The plaintiff, however, claims that despite the plain language of the agreement it may continue to manufacture and sell without making the payments required by the agreements because the formula which its predecessors acquired is no longer secret. To sustain this position plaintiff invokes the shade, if not the substance, of the traditional common law distaste for contractual rights and duties unbounded by definite limitations of time and argues that absent a construction that the obligation to pay is co-extensive only with the secrecy of the formula, it must be a forbidden "perpetuity" which the law will not enforce. I find no support for the plaintiff's theory either in the cases which it cites or elsewhere.

Thus, I hold that under the agreements in suit plaintiff is obligated to make the periodic payments called for by them as long as it continues to manufacture and sell the preparation described in them as Listerine.

In plain English, this roughly translates into “pay up or shut up,” with the court additionally stating that if Warner-Lambert no longer wished to pay royalties, they could simply stop selling Listerine (a laughably bad option, as sales had grown from a pittance into millions.)

After several more points, the court concluded with:

Defendants' motions for summary judgment are in all respects granted. Judgment for defendants dismissing the second amended complaint will be entered accordingly.

It is so ordered.

This ruling is critically important. It guarantees that irrespective of other conditions, as long as Listerine is sold, the royalties will be paid. Full stop. You might have also noticed the word “defendants'”—plural possessive. If you check the court documents, you will see a number of defendants, i.e., royalty holders.

John J. Reynolds, INC. purchased a half interest in the original royalty agreement several years prior to the federal suit. Other slivers were chopped up as well. Over the years since, portions of the original agreement have been further split amongst heirs and sold to and between private investors, pension funds, university endowment funds, and others.

In 2000, Pfizer acquired Warner-Lambert Pharmaceutical, which then in 2006 sold its Consumer Healthcare division to Johnson & Johnson. Johnson & Johnson has manufactured and distributed Listerine since and thus has paid out Listerine royalties as well.

A Piece of The Pie

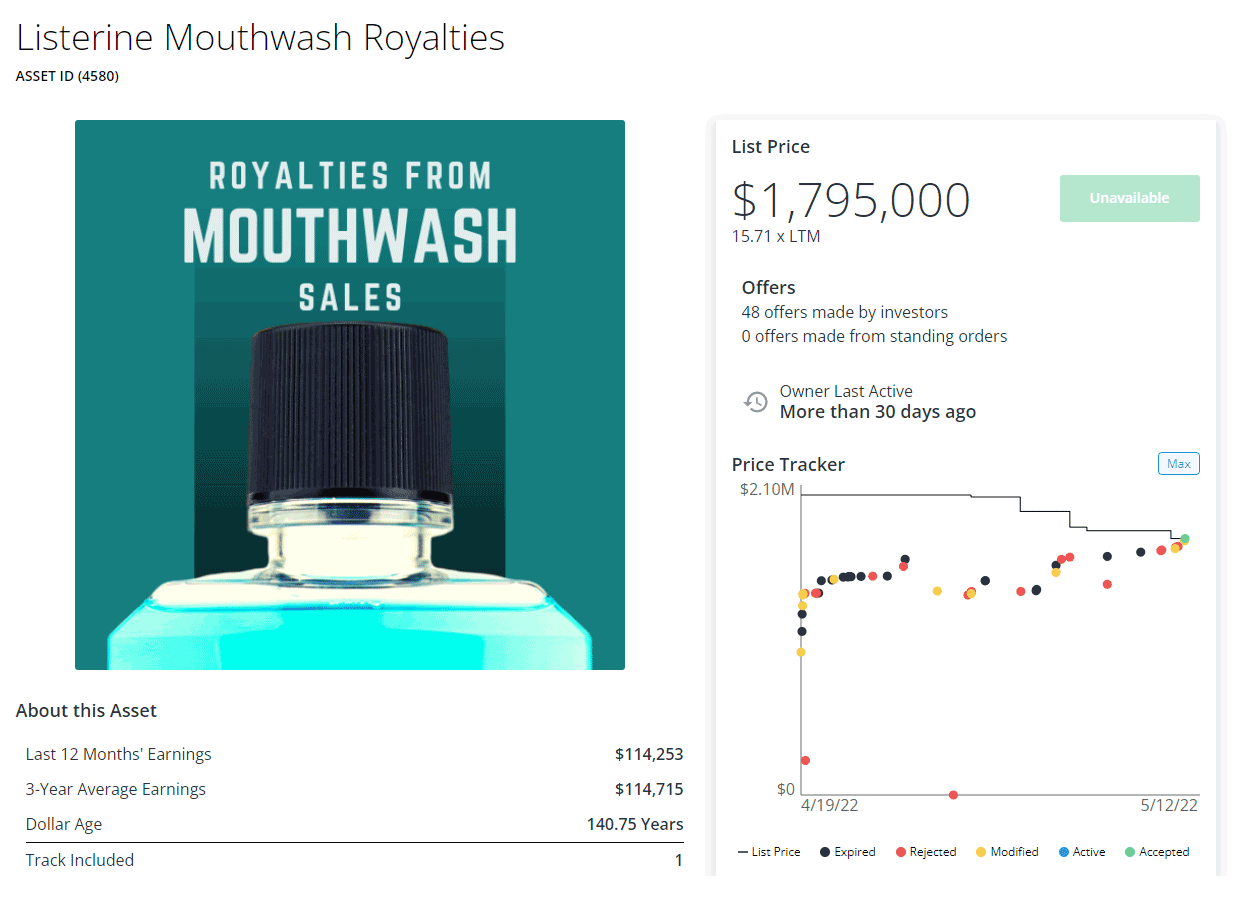

With an iron-clad court ruling, Listerine royalties represent a uniquely enduring cash-flowing asset. And every once in a while, one of the slices becomes available for purchase. In 2020, two separate listings were sold. Earlier this year, I discovered one on Royalty Exchange, a platform for buying and selling—yup, you guessed it—royalties.

This specific royalty slice was initially listed for $2.1 million. After about a month of entertaining offers, the seller accepted a bid of $1.795 million.

Does that seem overpriced? Under? You can run some quick math and divide the $114,253 in earnings by $1,795,000 to get a TTM yield of 6.36%.

It might sound appealing, but it really doesn’t tell you much. In fact, it really only tells you about the denominator in the calculation—the price a single person was willing to pay and the price the seller was willing to accept at a singular point in time. But what about the numerator—the actual earnings? And how would one go about calculating what Listerine royalties are worth?

Listerine Royalty Intrinsic Valuation

For starters, what something is worth is not strictly limited to what someone else is willing to pay. Fortunately, there are a variety of approaches to determining the intrinsic value of productive assets. This can be done for real estate, equity, and really anything that generates cash flows—like royalties.

But where to begin?

1. Defining the Asset

This asset entitles the holder to payments related to the global sales of Listerine, based on ounce volumes. The merits of this agreement are robust and have been upheld in federal court. From the perspective of JNJ’s obligation, we can think of this liability’s seniority as being in a weird capital structure purgatory, ranking below debt but above equity, as it is recognized by the product’s manufacturer as a cost of products sold. The asset is intangible, has no additional optionality, and has no liquidation value.

2. Estimating the Cash Flows

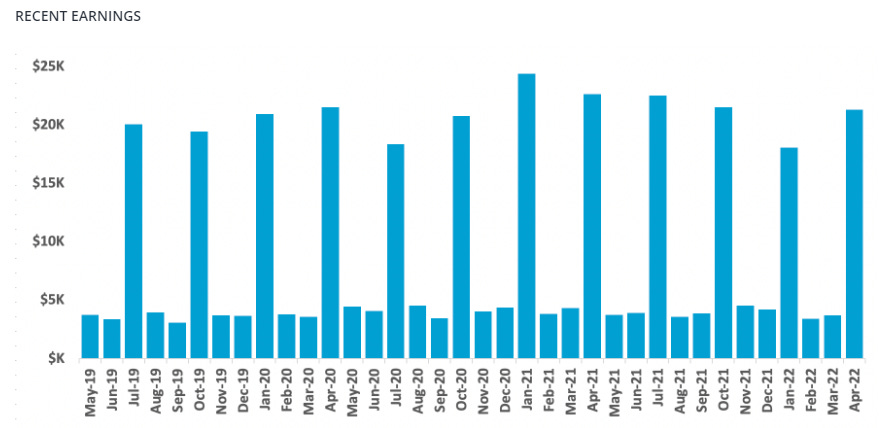

At the time of listing, this asset produced $114,253 in earnings over the last twelve-month period, .41% less than the 3-year average of $114,715. This indicates recent stability. When we break down paid earnings over the course of the years, things look slightly choppier, as domestic (U.S.) payments are paid monthly, and international earnings are paid quarterly.

3. Estimating the Life of the Asset

Many traditional royalties, like in the case of music, have a finite life of either 70 years after the death of the author, 95 years from publication, or 120 years from creation, depending. But as the 1959 court ruling clearly lays out, Listerine royalties must continue so long as Listerine is sold.

This asset is perpetual in nature and has an unlimited potential duration.

4. Identifying Additional Risks and Considerations

As the royalty payments are fixed relative to ounce sales volumes, any potential impairment to Listerine’s brand, loss of market share, a secular shift away from mouthwash usage, or other factors could negatively impact future payments.

A primary concern to the value of this asset is that the underlying agreement does not factor in inflation, with the royalties fixed relative to ounce sales volumes.

Royalties generated, including those from outside of the United States, are in USD.

Idiosyncratic risks for this asset include potential product lawsuits or failure of the ownership entity leading to the discontinuation of Listerine sales.

Lastly, there is not an active market to sell and purchase this asset, making it quite illiquid.

5. Forming the Narrative

The manufacturer and distributor of Listerine, Johnson & Johnson, currently holds the exceedingly rare AAA credit rating. However, the company has announced it intends to spin off its consumer healthcare division (which houses Listerine) in 2023. The credit rating agency Moody’s has stated this move may cause the resulting entity to lose its AAA rating, as liabilities tied to court rulings regarding tac product liability will likely remain with that segment. Even with a reduced rating, I believe the standalone entity will have a strong balance sheet, along with a variety of high-quality consumer brands, thus largely removing concerns related to ownership risk.

Listerine is one of only a short list of branded OTC antiseptic mouthwashes in the United States approved by the American Dental Association and has earned the ADA Seal of Acceptance1. Listerine also has years of comprehensive clinical research supporting the health benefits, as well as potential risks, of its use. This should greatly reduce concern around the possibility of future product lawsuits.

The royalty agreement being honored and paid for more than 140 years, as well as being upheld in federal court, removes concern regarding the continued validity of the asset. We have data highlighting the consistency in the income this asset generated over the last three years, but this is nowhere near sufficient to instill confidence for the long term. As this asset has a theoretically infinite duration, we need to understand the dynamics of ounce sales volumes.

Johnson & Johnson states:

More than one billion people in 85+ countries love LISTERINE® products for that clean, “yes, it’s working” feeling. A feeling that’s backed up by peer-reviewed scientific studies. More than 50 of them, in fact.

Listerine has proven itself as the number one mouth wash in the world, as evidenced by its large market share and growing sales. But how did Listerine become so popular? And can this popularity be maintained? It makes sense to look at what led to Listerine’s massive growth in the first place.

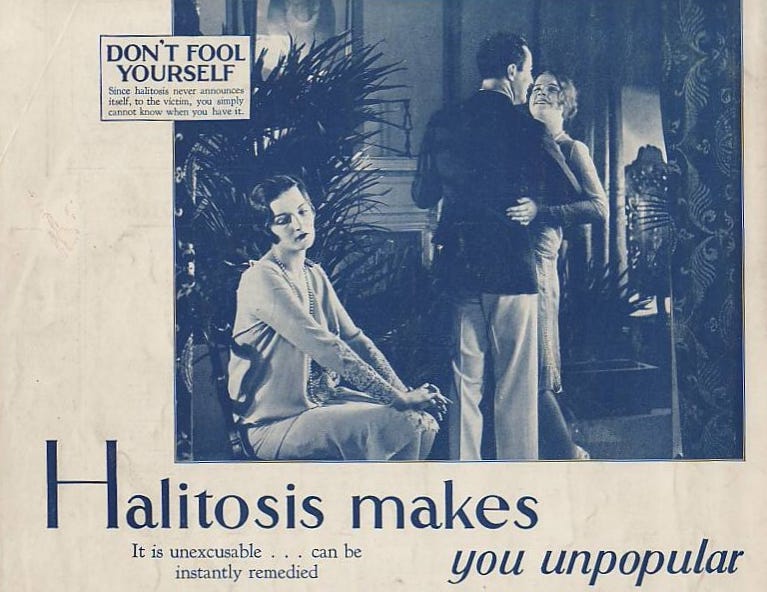

For starters, no one ever thinks they have bad breath. That makes it hard to convince people to buy a product that thwarts it. In 1920, Listerine began to leverage the term “halitosis” in its marketing. Halitosis, a Latin word derived from halitus (breathed air) and osis (pathologic alteration), simply means “bad breath.” It sounds scary, and the marketing worked.

Over the last century, the slow stream of U.S. Listerine sales has evolved into a sizable, steadily-growing river. And fortunately, the marketing strategy has evolved as well. Johnson & Johnson, backed by continuous clinical research on the product, has teamed up with media partners, retailers, and healthcare professionals to support the continued adoption of Listerine.

Interestingly, despite mouthwash not preventing COVID-19, concerns around the coronavirus plus a reduction in dentist visits boosted sales majorly, with 22% of those polled in the Sunstar Global Oral Health Awareness Survey reporting using mouthwash more regularly. While concerns regarding COVID-19 are abating, the increased consumer focus on oral health is expected to be a continued tailwind for mouthwash. With the boost, total global mouthwash sales experienced a ~4% CAGR from 2016 to 2020.

Currently, according to market and consumer data company Statista, approximately 200 million Americans (60.5%) use mouthwash. However, according to those surveyed in the Sunstar 2021 Oral Health Report, only 38% of Americans use mouthwash daily. From the same report, Spain and Thailand are tied for the highest, with 41% of their surveyed populations using mouthwash daily. On the other end of the spectrum is Japan, with a daily use rate of only 21%.

The space is nowhere near fully penetrated, and there seems to be a clear trend. But how fast will mouthwash sales grow in the future?

If you were aiming to map this out in the highest fidelity possible, you could aggregate data concerning historical trends and current penetration and usage rates for each country in the world, along with:

Population demographics (aging populations have increased dental disease and thus a higher propensity to use oral products.)

Diet habits (with a focus on the increase in sugar consumption globally.)

Current oral hygiene habits (especially mouthwash use and the prevalence of regular dentist visits.)

Controlled substance use

Marketing efforts/spending from major mouthwash brands.

Endorsements by organizations and health care professionals.

Quality of healthcare, government healthcare programs, and health education efforts.

Trends in sub-varieties of mouthwash.

Factors concerning the material sourcing, manufacturing, and distributing of mouthwash.

The list goes on and on.

You’d end up seeing that large countries like India represent giant opportunities. Much of the population does not have access to comprehensive oral hygiene products, and cavities and gum disease affects a majority of the Indian population. This has led to the government launching the National Oral Health Programme, as well as the Indian Dental Association starting initiatives for the education and promotion of mouthwash use.

If you were to conclude that mouthwash has long runways in both adoption and frequency of use, you would not be alone in your thinking.

According to several market data companies, total global oral care market sales are projected to grow ~6% per year from 2021 to 2030, with mouthwash experiencing a ~6.5% CAGR over that same period. Though without seeing the exact methodologies used, it’s worth taking this with a grain of salt.

To avoid missing the forest for the trees, It’s likely beneficial to distill the narrative down into a few key concepts:

The global median age is expected to continue to increase. Older demographics tend to use mouthwash more.

As oral health education, marketing, and product accessibility increase globally, so will mouthwash adoption and use frequency.

Listerine is the top global mouthwash and will continue to grow brand affinity and will likely retain substantial retail share.

6. Aligning the Inputs

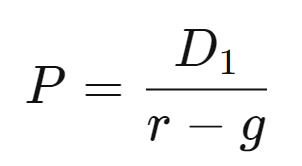

The easiest approach to calculating the intrinsic value of an asset like this is the Gordon Growth Model (also known as the dividend discount model), with a few minor adjustments.

g = Perpetual growth rate

r = Stable cost of equity (hurdle rate)

D1 = Value of next year’s dividends

P = Current stock price

Input - g

While mouthwash sales are expected to grow at a mid-single-digit rate until 2030, that is likely far above what will be achievable perpetually. Furthermore, the established pricing power held by Listerine does not impact the growth of the royalty payments, as they are fixed on ounce volumes sold. Therefore, to be conservative, it may make sense to use a value of ~1% to account for global population growth. This assumes Listerine holds its approximate market share but discounts any positive trend in use frequency. Overall, this likely understates the payments of the next decade but helps avoid creating an overly-positive picture.

Input - r

For traditional equities, the stable cost of equity would be calculated using the CAPM, CoE = Rf + β * ERP. Since this asset is not equity, proxies will be needed for some of these values. Alternatively, you could skip going through the motions and use your own determined hurdle rate.

The Rf, or risk-free rate, will be the US30Y treasury, currently yielding 3.3326%.

Getting a beta is trickier. This asset isn’t an equity share, and the returns look uncorrelated to traditional equities. Unsurprisingly, that’s why institutional investors would gravitate towards an asset like this: exposure would, in theory, push the overall volatility of the portfolio down. For lack of a better idea, JNJ’s 5-year beta of .66 will have to do.

ERP, or equity risk premium, reflects the additional return above the risk-free rate necessary to justify a riskier equity investment. We’ll use an MMRP—a modified market risk premium— by taking an approximated ERP of 5.7% and tacking on an extra 1% to buffer against some of the highlighted risks.

Input - D1

The “value of next year’s dividend” is pretty straightforward. The dividend, in this case, is simply the royalty payment. Take last year’s earnings of $114,253 and use our estimated perpetual growth rate of 1%, and it results in $115,395.53.

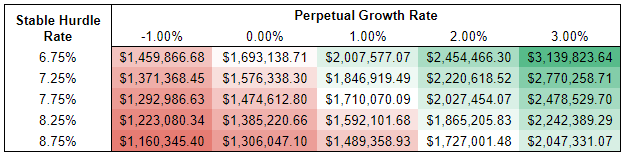

7. The Output

P = ($114,253*(1+.01))/((.03326+.66*.067)-.01)

Below are values implied by a range around the estimated inputs:

Surprisingly, the $1,710,070.09 implied value is only off by about 5% from the $1,795,000 winning bid and suggests a fair value of ~15x LTM earnings. But as you can see, the implied values change drastically with shifts in the hurdle rate and growth rate. We also failed to include a critical consideration: illiquidity. For a large fund, the fact this asset is illiquid would likely be of little concern. But for an individual who would be highly concentrated in an asset like this, it might warrant discounting the value further, by 10% to 20%, for example.

Did the bidder overpay? Was our math off? I don’t think either is the case.

Valuation isn’t a precise science; it’s an art.

While we (rightfully) attempted to be conservative with some of our estimates, there is plenty we still don’t know. Maybe the buyer had more information to work with, or perhaps they simply had a lower hurdle rate than us. There’s even a chance that the purchaser was an individual who just wanted to own a unique asset—a piece of history, and wasn’t concerned with overpaying for the bragging rights.

Are Listerine Royalties a Good Buy?

It’s clear why investors, namely certain institutions, would be interested in buying Listerine royalties. When yield has been hard to come by for years, this asset offers steady, uncorrelated cash flows. Furthermore, the royalty payments are in USD, even for sales outside the U.S., which may be largely beneficial if the USD continues to show relative strength. There’s also an odd tradeoff between the payments not being linked to inflation while avoiding negative pressures from increased input costs for the underlying product. Notably, the royalty payments are pre-tax income, and as this is a perpetual royalty, there don’t seem to be any solid tax advantages, especially compared to real estate.

I’ll continue to dig around to see what else I can find out about this unique asset, and I’m keeping my eyes open for when another listing pops up. If I saw a small slice at a price I thought was a steal, I’d probably be a buyer. But as of today, I’m more than happy watching from the sidelines.

As always, thanks for reading. If you enjoyed this article, please show your support by subscribing and sharing my work with others.

Disclaimer

This publication’s content is for entertainment and educational purposes only. I am not a licensed investment professional. Nothing produced under the Invariant brand should be thought of as investment advice. Do your own research. All content is subject to interpretation.

Additional References and Resources:

Sunstar, Global Healthy Thinking Report, Oral Health Awareness Survey, a worldwide consumer study on oral health and dental care. 2021

Marco A Peres and Al. Oral diseases: A Global Public Health Challenge. Lancet. 2019

United States Census Bureau. U.S. and World Population Clock Website.

Data on File, Johnson & Johnson Consumer Inc.

Marcenes W, Kassebaum NJ, Bernabé E, et al. Global burden of oral conditions in 1990-2010: a systematic analysis. J Dent Res. 2013

Edited 7/27/2022. Originally claimed Listerine was the only OTC antiseptic mouthwash to have earned the ADA seal of acceptance. The Source of the original claim can be found here. A full list of such accepted products can be searched here.

Tags: JNJ 0.00%↑ PFE 0.00%↑

This reminds me of the old Forbes magazine. Quite interesting.

This was a great read, thanks Devin!