United-Guardian: Welcoming Instability

“We are pleased to announce that sales increased by 27% for the first quarter of 2024 compared with the same period in 2023. Cosmetic ingredients saw the greatest increase with sales up 146%.” - Donna Vigilante, United-Guardian President, Q1 2024 Press Release

Having last written about United-Guardian in December, the calendar would say that an update is long overdue. Despite a relatively strong Q1’24, the nanocap pharmaceutical and cosmetics company still faces an undeniable mix of challenges, and the resulting financial performance has not been all too impressive when compared to just a few years prior. However, as always, tucked in between are considerations worthy of exploration.

In December of last year, covering through Q3’23, I wrote:

While these net results appear far from stellar, there is a key point to note:

In the first nine months of 2023, United-Guardian generated EPS $0.01 lower than what my most recent model showcased for the full year 2023. At the same time, the model showed CI and ML sales for the full year close to what was achieved in the first nine months. This is the result of being conservative with inputs and, as always, using models to illustrate and understand potential outcomes rather than attempting to predict with precision. UG is now positioned to likely generate near $0.50 EPS for the full year—right between the June and August models.

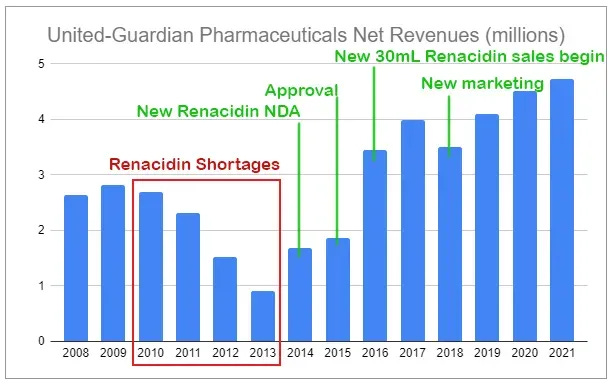

Full-year results were indeed strong relative to the weak model I had previously illustrated. Net revenues of the CI and ML segments, predominantly Lubrajel, were reported as down 20.04% and 29.13%, respectively. Gross margin came in softer than the year prior—no surprise as the sales mix shifted toward lower-margin Pharmaceuticals. And unlike previous years, in which Pharmaceuticals steadily grew, segment net revenues were near-flat with an increase of 0.14% from the year prior. This unenthusiastic performance was not due to a lack of demand for the product but rather was an issue with supply—telegraphed far ahead of time, also noted in December’s piece:

Posing as a clear risk to the segment, in mid-October, United-Guardian informed the FDA of a potential supply shortage of Renacidin. Amsino Healthcare, the manufacturer contracted to produce Renacidin, will be temporarily ceasing manufacturing of the product due to required facility maintenance. This appears nearly identical to the Renacidin shortages of 2010-2011 due to issues with the previous contract manufacturer. Amsino has disclosed that due to the shut down two orders originally set for December 2023 and January 2024 will be pushed to early February 2024.

At the same time, operating expenses and R&D were modestly lower, ultimately resulting in a reported EPS of $0.56, in line with the year prior, despite mounting pressures. However, there is a clear caveat. While 2023’s results included a sizable increase in investment income, up some 29.5% from the year prior, 2022’s figures included a $1 million realized loss on the marketable securities portfolio. Stripping out that loss would have resulted in the previous year’s EPS being $0.79, 41% higher than otherwise, and unmistakably highlighting the true degradation of core operations.

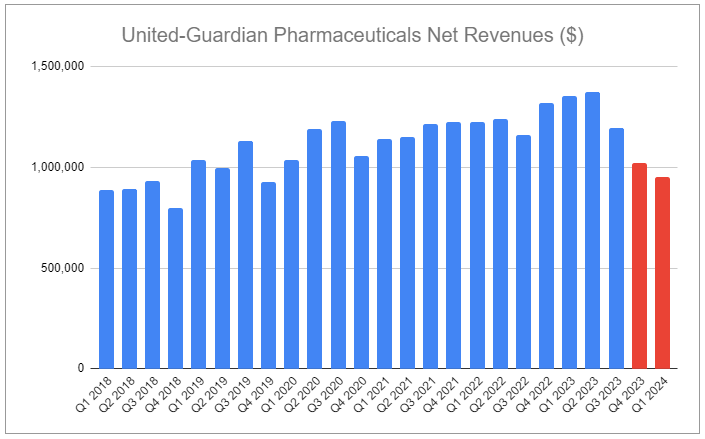

Q1 of 2024 showed a very different mix of results. The Renacidin shortage persisted, resulting in Pharma net revenue being down 29.83%, a notable decline following the Q4’23 drop of 22.51%. While it would be easy to extrapolate such a decline straight towards zero, such expectations are likely quite far away from what the rest of 2024 has in store. For one, and most importantly, announced by the company in May, the production of Renacidin has fully resumed, allowing orders to be filled in their entirety. Secondly, though far less consequential, is United-Guardian’s other Pharmaceutical, Clorpactin WCS-90, which is a low percentage of segment net sales but grew by ~8% in Q1. In all, the segment headwind was all but temporary and far less lasting than previous shortages. For context, I point to the previous chart highlighting prior shortages versus the more recent quarterly segment net revenues. Four months is far different than four years:

Other segment sales also showed a very different picture in Q1’24. Unlike the previous two years, when there was a large glut of stock that customers needed to work off, Cosmetic Ingredient net revenues increased by 146%, largely driven by ASI, the company’s largest distribution partner meeting demand in China. Medical Lubricants, while nowhere near as stellar, did not continue the precipitous decline experienced the year prior, with net revenues up roughly 2%. Alongside expenses kept at bay, the company recognized a substantially higher investment income figure, courtesy of shifting its portfolio of marketable securities toward higher-rate treasuries, exceeding a lower net gain on marketable securities and sending EPS 25% higher than Q1’23.

Several factors have the potential to drive results similarly higher throughout the rest of the year. However, demand for Cosmetic Ingredients has been extremely lumpy due to industry dynamics within China, and results are far more a function of ASI’s work than UG’s. A more distinct possibility, and one that is far more likely, is Pharma's performance exceeding the recovery in Renacidin net sales, driven by the company’s efforts to raise awareness of the product with doctors and other medical professionals. Second is the company’s Sexual Wellness category, comprised of natural variants of Lubrajel, which have been fully developed but no commercial sales made—yet. Based on the timing of UG’s announcement of entering a distribution agreement with Brenntag, it is quite conceivable that the company will begin to receive related orders in H2’24. While the extent of the demand and potential contribution can not be fully quantified, it is likely the Natrajel line is near the highest margin across the company’s product portfolio.

To further drive sales in both CI and Pharma, UG hired a new marketing director in May. Along with this, the company’s 2023 total dividend was substantially lower than years prior, not only to retain enough cash to keep equity above NASDAQ listing requirements but presumably to have extra resources to devote to new marketing avenues. While this culmination of efforts does mark a new growth orientation for the company, it is not exactly surprising. What is surprising is the fact that the company is still operating without a CEO, following the short tenure of Beatriz Blanco—a position the company shows little interest in changing. The company is essentially being run by Donna Vigilante, President, who has worked at the company for decades, overseeing R&D, alongside the heavy influence of Ken Globus, previous long-time CEO and still current chairman of the board of directors.

While the company’s Q1’24 press release claimed a hopeful stabilization for CI and ML products, I remain unconvinced that sales will revert to their previous substantial contributions, especially with the lack of an active CEO at the helm. Rather, Pharmaceuticals remain positioned as the principal star segment, manufacturing hiccups notwithstanding. With higher investment income from a growing cash balance and zero debt, there is a value that could very well become markedly mispriced by the market.

With only a trivially small tracking position, the core thesis remains to wait for an even more pronounced mix of headwinds to create a price entry that more than offsets the immense uncertainty surrounding the company. The company continues to provide sparse information publicly; there is no additional analyst coverage, limited liquidity, and merely 355 shareholders on record. Should China sales weaken, growth initiatives stall, and any major shareholder substantially trim, there is little friction to stop the share price from finding its way below the 52-week low of $5.79—a long but easily reachable distance from Friday’s closing price of $8.94. Currently, cash and marketable securities make up 23.17% of the market cap. Such an opportunity may never present itself, but it should be no surprise if such a setup occurs within the next 5, 10, or 20 years. A revised model is provided for illustrative purposes. It includes stale CI and ML sales, modest growth in Pharma, growing investment income, an elevated ETR, and an equity multiple stable at current levels. Instability is most welcome.

Future notes on UG will become even less frequent—opting to shift a portion of time toward highlighting similarly obscure assets with unique considerations.

If you enjoyed this piece, hit “♡ like” on the site and give it a share. To further show your support, consider pledging a paid subscription to Invariant.

Ownership Disclaimer

At the time of publishing this piece, I hold positions in United-Guardian.

Disclaimer

This publication’s content is for entertainment and educational purposes only. I am not a licensed investment professional. Nothing produced under the Invariant brand should be thought of as investment advice. Do your own research. All content is subject to interpretation.

Tags: UG 0.00%↑ ASH 0.00%↑

"opting to shift a portion of time toward highlighting similarly obscure assets with unique considerations"

Looking forward to it! :-)

You still follow this one?