Haypp Group: Acceleration

“The demand for our enhanced services continues to grow significantly, enabling us to provide even better consumer offers in 2026. As I underlined in earlier quarters, the sustainability of our gross margin is the foundation for our global and U.S. growth strategy, enabling the investments required to build the next chapter.” – Peter Deli, CFO, Haypp Group, Q4’25 remarks

The U.S. market, the greatest opportunity, which Haypp continues to prioritize, is growing radically. Haypp has regained an advantageous direct supply of ZYN from Philip Morris International. We have witnessed market fragmentation, with British American Tobacco’s Velo Plus (along with reformulated Grizzly) taking nearly a quarter of the market in record time. Industry pouch volumes (offtake) grew by 35% y/y in Q4, and 32% in January 2026. on! Plus has been authorized through the FDA’s pilot program. We have no way of knowing if or when other authorizations will come, but the environment is already favorable for Haypp. If Velo Max and ZYN Ultra are both authorized, the environment moves closer towards ideal.

More high-quality products, appealing to a wider adult audience, will support the continued growth of the category. The physical limit of shelf space at c-stores means the widest assortment will be available online. Scale, and the absence of additional costs associated with physical distribution and retail, will mean that Haypp remains able to sell at remarkably low prices. This is especially so when its Media & Insights business provides high-margin dollars that can be used to subsidize the proposition presented to consumers.

Haypp’s new consumer acquisitions in the U.S. have heated up too, growing by 195% y/y in Q4’25 and 58% sequentially from Q3’25. Not shown in the figures, but disclosed by the company, January 2026 shows pouch volumes up 120% and new consumer acquisitions up by more than 250%. Staggering. Naturally, but perhaps overlooked, is the fact that new consumer acquisitions can not be extrapolated into immediate revenue growth 1:1. The majority of sales are made to existing consumers, with mature, ingrained usage and purchase habits. New consumer growth hints at what is to unfold over multiple quarters and years.

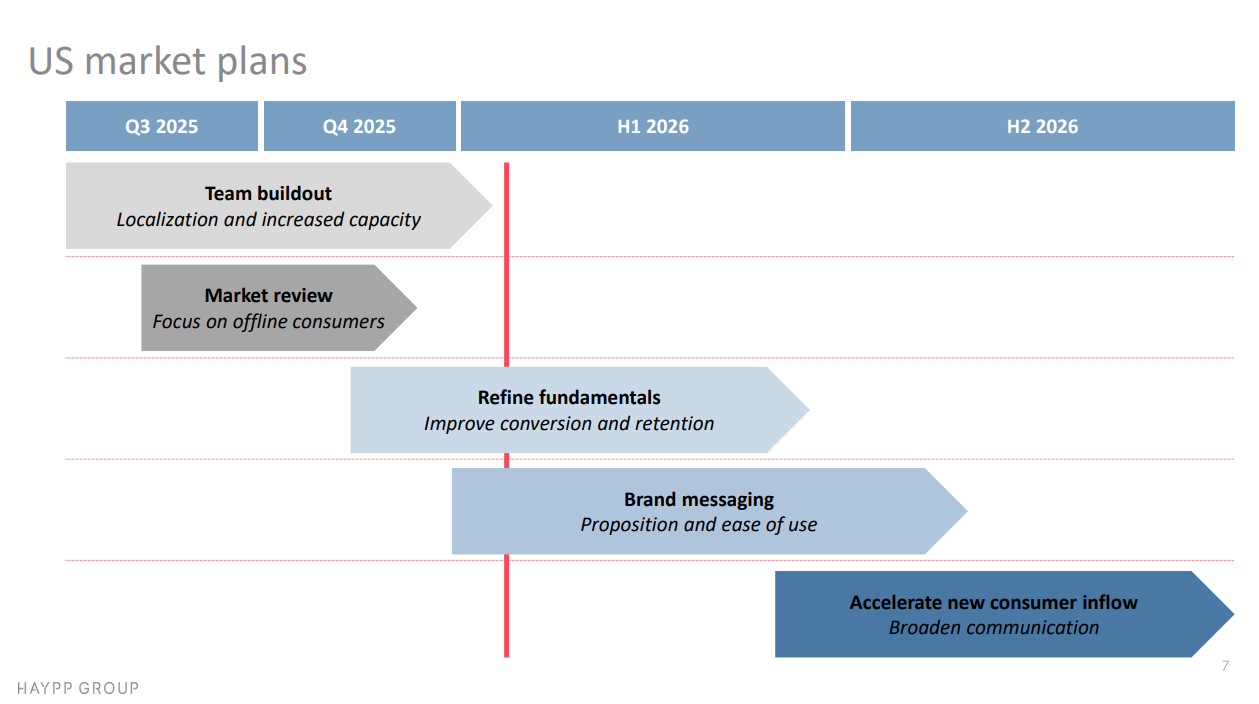

Haypp sports remarkably high retention, and both retention and new consumer acquisition conversion rates are improving. These efforts were tackled in earnest in Q4’25 by the new U.S.-dedicated team and are expected to continue through H1’26, as illustrated on slide 7 of the Q4’25 presentation. Once refined, the company will then deploy resources to accelerate new consumer acquisition. This is absolutely the correct order and the route I have advocated for. As highlighted last quarter, the company’s new loyalty and referral programs can act as a dual engine for growth. I have seen little discussion elsewhere on these programs, but I expect them to gain serious attention. Each fully refined prior to engaging in more significant marketing can provide an outsized amplification of all dollars devoted. Focusing on near-term Growth Markets margin compression is missing the forest for the trees.

Given the size of the opportunity, it’s understandable that Growth Markets, primarily the U.S., receive disproportionate focus. However, Haypp’s Core Markets can not be overlooked. Core net revenues grew by 6.2% in FY’25, driven by strong growth in nicotine pouches, partly offset by the decline in Snus. Critically, full-year segment EBITDA margin expanded by 160bp to 10.3%, and was at 10.5% in Q4. This segment comprises highly competitive markets, including Sweden, where Haypp holds just over 30% of the total category share. Sweden is also second to none when it comes to positive pouch regulation, providing minimal risk from the government. Usage trends shifting from snus to pouches, usage occasions rising, and pouches accounting for a greater share of total sales support a modestly improving net sales growth rate. FY’25 net sales compounding at a 7% rate through 2028 results in SEK 3.4 billion for the segment. While we should not assume segment margin expansion in 2026, there is a clear path to modest margin expansion, driven by scale and M&I, to between 11-12% in 2028, resulting in segment EBITDA of approximately SEK 400 million. In other words, the company currently trades at ~14x 2025 Core markets EBITDA and just over x10 for 2028, ignoring the vast potential of the U.S. and beyond.

Hidden amongst

In February of last year, I noted how Haypp’s underlying financials have always been hidden to a degree as the business has expanded. Declines of snus masked the growth of pouches in Core Markets. Losses in Growth Markets obscured the Core's profitability. How exactly those Growth Markets were growing was masked by declines in legacy oral tobacco products that also carried weaker unit economics. After Growth Markets became profitable, the new Emerging Markets segment began eroding the group’s profitability.

These developments are mostly straightforward. They weren’t detectable if you were looking at Haypp through a basic screen, but became evident once you started digging through the company’s reports. But these are not the only factors that have muddied the waters. Ending sales in California and pausing sales in other select states contributed. The ZYN shortage, which initially drove users online in search of the beloved product, reversed. Haypp was forced to ration its inventory, capping allowable amounts per order. Then, when Haypp ran out and could no longer source directly, there was a nontrivial level of churn among those new cohorts.

The recent reacceleration of new users and pouch volumes in the United States is partly attributed to Haypp reestablishing a direct ZYN supply from PMI. However, the implications aren’t wholly straightforward, and not all metrics, at face value, appear positive for Haypp. Another mask has been layered on. To explore that, we must first consider what actually occurred because of the ZYN shortage.

Revisiting the button

On May 11, 2025, I posed a question: Pretend there was a button you could push that would ‘erase’ the ZYN shortage. Ignore the effect on PMI and all other industry participants and only concern yourself with how it would affect Haypp. Would you press the button?

I believed most people would immediately slam that button. My personal perspective was quite different (emphasis added):

The absence of U.S. ZYN is captured in Haypp’s top line and the number of active consumers in Growth Markets. All else equal, it would be preferred if those figures didn’t experience a drop—an eventual resumption of ZYN sales would be unmistakably positive for the group, as not having a popular product available diminishes the value proposition. However, as I’ve highlighted over the last month in notes on Haypp Group’s 2025 CMD and the Q1’25 results of Philip Morris International and Altria, the U.S. market is becoming more fragmented. This is one of the most essential and beneficial dynamics for Haypp. The ZYN shortage has unmistakably accelerated growth rates of new competing brands. I believe that, even with ZYN normalizing channels in H2’25, there is considerable momentum behind other brands. While they are nascent, I expect them to continue to take share. Cracks will spread. This is ideal timing for Haypp to significantly ramp up investment into customer acquisition and raise awareness of the online channel.

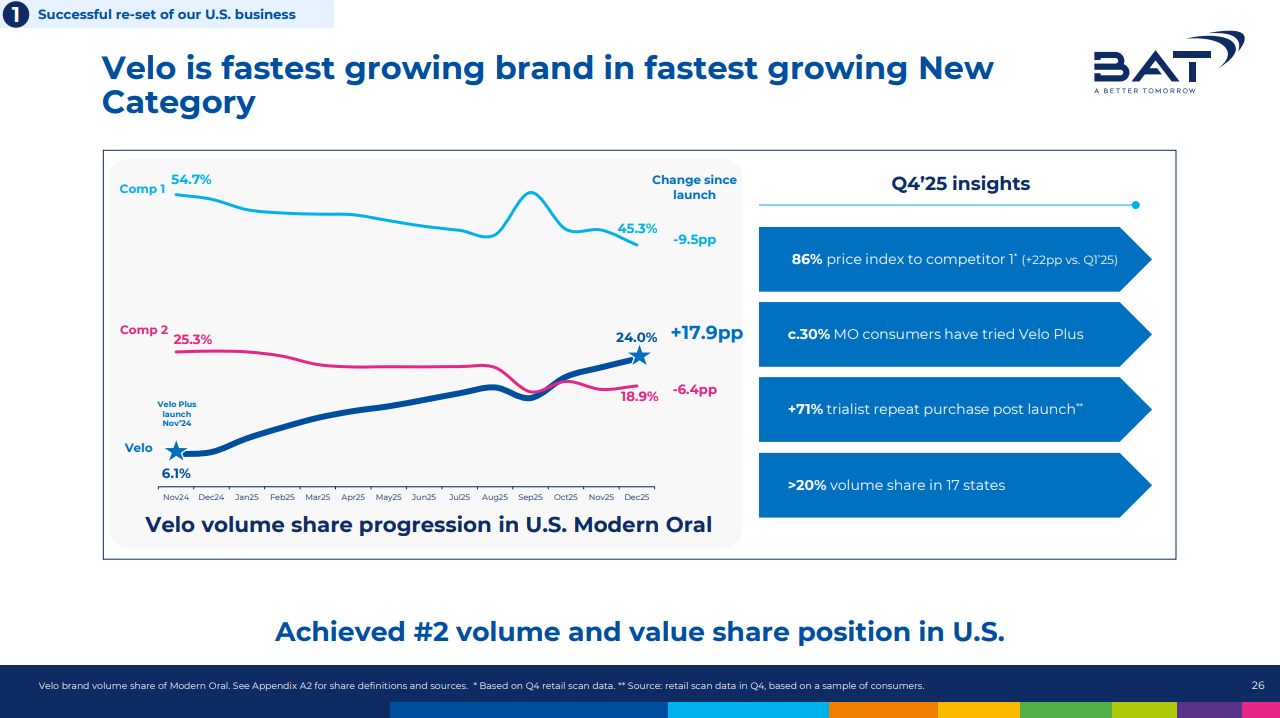

Fre/Alp, zone, and other brands were aided by the wavering absence of ZYN. No brand benefited more than Velo Plus.

You might question how much Velo Plus benefited, given its launch came after the most intense period of the ZYN shortage. However, I will steadfastly argue that Velo Plus had a far easier time generating product trials because many users, previously accustomed to using ZYN exclusively, had already changed their behavior and had trialed other products. The quality of Velo Plus led to significant repeat purchases. The only reversal in market share trend was when PMI initiated temporary, but intense, promotions.

The U.S. market has changed.

Despite the short-term headwinds that hit Haypp, the ZYN shortage was a phenomenal boost for the company’s long-term trajectory in the United States. We are only starting to see the effects. But one of those effects is again shrouding the underlying trend.

When Haypp was affected by the ZYN shortage, its consumers shifted to other products that carried lower ASPs. This had a direct, negative effect on average order value and net revenues. However, those products also carried higher margins, allowing Haypp to more than offset the impact at the gross level. While exact details aren’t disclosed, we know that the reestablished direct ZYN supply is now more comparable to the margins of other products. Despite this, due to the fragmentation that has occurred and the persistent heightened competition among brand owners, it is also priced lower than it was pre-shortage, which again has a negative effect on AoV and net revenues.

on! Plus, having received FDA authorization for a number of SKUs, is confirmed for a nationwide rollout beginning next month, with broad retail distribution by the end of H1’26, as Altria confirmed during its 2026 CAGNY presentation. Even without additional authorizations through the FDA’s accelerated pilot program, this will again increase competition and overall promotions, potentially leading to temporarily lower ASPs for Haypp, further masking the underlying evolution. This will coincide with the company’s higher rate of reinvestment into its Growth Markets.

Pushing on the gas

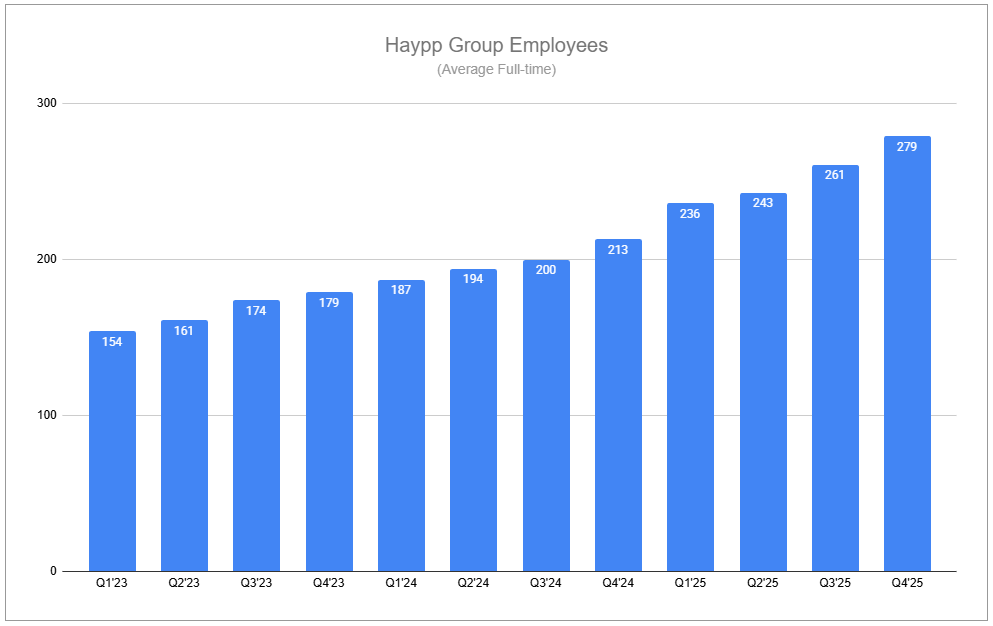

Despite turbulence within the U.S. market throughout 2025, Haypp wasted no time working to capture the ever-growing opportunity. The year was marked by the buildout of the U.S.-dedicated team, which was the primary driver of the significant increase in headcount.

The company also conducted intensive research to determine the most effective way to raise awareness of the online channel and to tailor Haypp’s value proposition to consumers. Improved site infrastructure has allowed for greater iteration and customization, and the company is actively refining how it communicates with consumers and presents its value proposition.

In the middle of slide 7 of Haypp’s Q4’25 presentation sits the marker “Refine fundamentals.” This includes a host of things such as navigation, highlighting special offers, checkout, shipping rates, and numerous other aspects that factor into the user journey. It also covers the company’s still-nascent referral and loyalty programs. Regarding what exactly these programs entail, I point you to last quarter’s note.

I will say, in and of themselves, referral and loyalty programs offer nothing of significance. Provide a poor product or service? Charge too much? People are unlikely to repeat their purchase. They are even more unlikely to refer their friends and family to you.

There is a counterargument to the opposite: if you provide exceptional value to your customers, why on earth would you need referral or loyalty programs? But such a line of thinking misses the point of Haypp’s scale economies shared model. As I laid out in my Q2’25 note, Skyward, with ‘Never enough’, pushing on the gas is what produces greater value for all parties. I expect these programs to be extremely impactful, along with other systems the group is meaningfully investing in.

Insights on Media

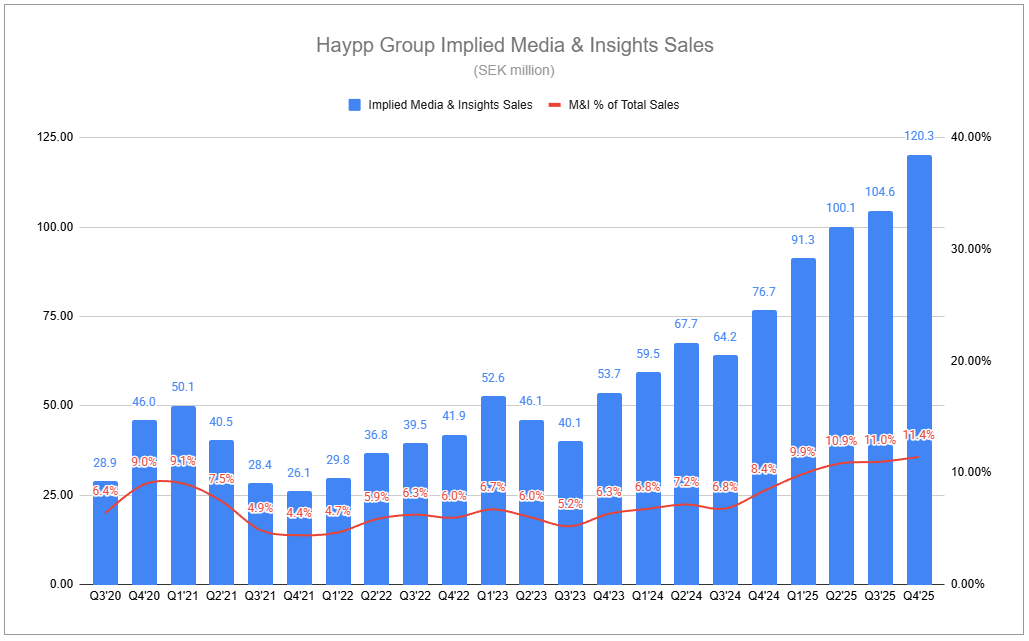

The importance of Haypp’s M&I business can not be overstated. It is critical not only for funding growth but also for providing incremental high-margin dollars that sustain low unit prices for pouches. Outpacing the rest of the business, implied M&I sales grew by 55% in FY’25.

Understanding the growth drivers behind the Insights side is fairly straightforward. More brand owners competing equates to more demand. Demand from regulators and academic bodies is also growing. More consumers reinforce the quality and value of the Insights data.

The Media side has its own straightforwardness. As competition intensifies within a geography, brand owners become more willing to spend more on media placements. This includes anything from sponsored listings to banner ads. As the number of consumers using Haypp’s sites increases, the value of media placements increases. But there was previously a concern. Over the last two years, we have seen total media placements increase across Haypp’s sites. That’s certainly good for driving incremental Media sales, but there is a ceiling. You can only increase placements so much before the density is overwhelming and degrades the user experience.

Haypp’s management has stated that M&I demand going into 2026 was robust. But Media is bound to provide an increasing contribution as the group actively enhances its Media offerings. Historically, Haypp’s Media offerings have been primitive compared to large-scale, established platforms in other industries. This is changing meaningfully.

Keep reading with a 7-day free trial

Subscribe to Invariant to keep reading this post and get 7 days of free access to the full post archives.