Imperial Brands: Mechanical Animal

“We have a healthy respect for our competitors and their own ability to innovate. But we are building a track record that gives us more confidence that we are now a more resilient, more agile business than we were in the past. And as we look at our pipeline of transformation initiatives, there’s more upside to come. And this future upside is an important part of our investment case. We are building a stronger tobacco business.” - Stefan Bomhard, Imperial Brands CEO, FY’23 Call

Imperial Brands is years behind in the race for next-generation products. Now, citing a myriad of reasons, declines in its tobacco volumes have appeared to accelerate. Adding fuel to the fire, NGP operating losses grew year over year for FY’23. Despite all of this, I find myself in agreement with the CEO’s central outlook featured above.

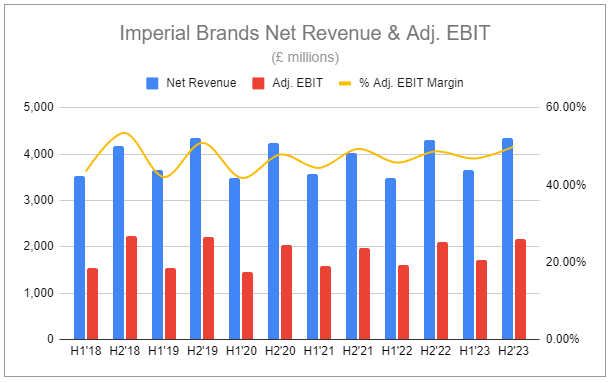

2023 reported tobacco volumes decreased by 10.37% y/y. However, normalizing 2022 by subtracting out Russian volumes shows remaining associated volumes falling by 7.09%—meaningfully lower, albeit still substantially higher than the normalized 1.2% drop in 2022. Worthy of note, In 2023, Imperial gained incremental share in the United States, Spain, and Australia, with positive aggregate share change across priority markets.

Additionally, within the Americas reporting geography, while tobacco volumes decreased 6% y/y, 4% was attributed to mass-market cigars due to wholesale inventory movements, signifying a mere 2% drop from related cigarette volumes while the industry declined by roughly 8-8.5% for the period. The relative strength stems from the performance of discount brands—a recent headwind for Altria. Stefan Bomhard, Imperial’s CEO, touched on this dynamic during the call (emphasis added):

I feel very confident in our delivery in the year, and you've seen about a lot of the upper levers that we are pulling at this point in time. And I think I come back to the point the question asked before about one of the benefits we have at Imperial is that we have a brand at every single price point in the marketplace in every one of our top 5 markets. So we are in a position to serve our consumers at every single price point. And I think that is a differentiated competitive advantage in today's world.

One would be wrong to focus on volumes or share without offering the context of pricing, which in 2023 was double digits across all reporting geographies, driving positive net revenues and adj. operating income across the board. Additionally, the positive performance of Logista drove associated distribution income higher, reflected in the total below.

Logista: The Distribution Pillar of Imperial Brands

Group EBIT growth was despite NGP losses increasing by 48.3% in 2023. But it’s essential to understand the evolution of associated losses. In 2020, Imperial essentially gutted and revamped its NGP offerings, recognizing EBIT losses exceeding associated net revenues courtesy of £124 million in write-downs in inventory and IP. The company has since taken an extremely cautious approach to rolling out new products. Critically, it has no intention of being the market leader in any NGP category. Rather, it is unglamorously riding coattails as others (principally PMI and BAT) spend significant money to develop markets and raise consumer awareness—only entering once specific product categories become established. This strategy is likely to ensure a significantly smaller share of the market, but, in its nature, will do so at a significantly lower cost. With this in mind, it’s key to note that the expanding losses in 2023 were largely the result of market launches.

NGP net revenue growth has accelerated, up 26.4% as a group in 2023, and up 40.4% in the Europe geography for the period, with offerings in all three NGP categories (Vapor: blu, HTP: Pulze, MONP: Skruf, Zone X).

Imperial is guiding to NGP losses shrinking and reaching breakeven in 2025. This appears ambitious, perhaps overly so, but management has affirmed its guidance even considering the Modern Oral Nicotine Pouch rollout scheduled for 2024 in the U.S.—an endeavor certain to carry non-trivial costs. FY’24 guide now includes LSD net revenue growth, Adj. EBIT growth ‘close to middle’ of MSD range (~4%?), with higher interest and tax rates partly negating the benefit of share buybacks and profit growth on EPS, and for total performance to be H2 weighted, due to lapping 2023 pricing and NGP investments being weighted to H1. It is clear the market is expressing significant doubt regarding Imperial Brands’ long-term viability as a going concern. As of Friday's closing price of 1852p, it trades at ~6x EV/aEBITDA and 6.4x adjusted earnings and is set to return more than 14.5% of its current market capitalization to shareholders in 2024. NGP growth stalling out? Competiting NGPs eating share from Imperial’s legacy offerings? Interest rates perpetually suppressing earnings?

For illustrative purposes, assuming:

Group EBIT growth comes in marginally softer than guided for FY’24.

Sluggish NGP growth and weaker pricing fail to offset legacy tobacco volume declines, leading to Tobacco & NGP EBIT degrading at a gradual pace evolving toward rapid.

Logista growth, a function of organic pricing and M&A, declines to 3%.

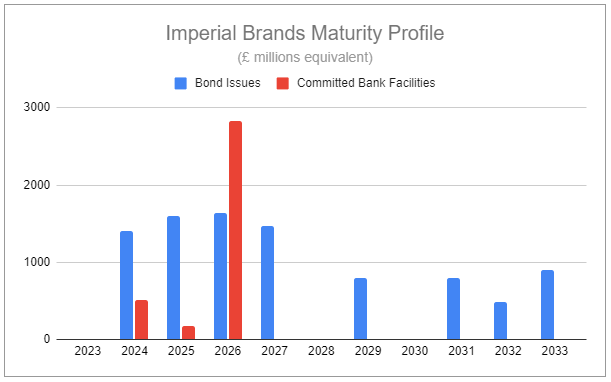

Net financing costs continue to significantly expand as notes are rolled forward.

Tax rate evolves toward 23.5%.

Dividend increases by 2% per annum; half of the forward guide.

Annual share repurchase program remains fixed following £1.1 billion in 2024.

In the hypothetical, over the next decade, Tobacco & NGP EBIT, Group EBIT, and Adj. Net Income decrease by 22.5%, 16.5%, and 28.3%., respectively. At the same time, Logista grows from 7.8% to 14.5% of Group EBIT. Over the decade, sustained share repurchases retire nearly two-thirds of shares outstanding, resulting in Adj. EPS doubling and the dividend per share increasing by 22% off of a base of 8.1% while the payout ratio falls from half to a third of Adj. Earnings. Despite the lofty and growing dividend, total dividends in absolute terms actually decrease, from £1.3 billion in 2023 to £590 million in 2033.

The above input assumptions provide substantial leeway for Imperial Brands to deliver operational performance well above what is illustrated. Constant growth in the core business is not required. A small improvement to the aggregate Group EBIT decline rate or even several years of prolonged stability radically alters the total capital available to return to shareholders. Additionally, it is quite likely that Logista will grow at a more elevated rate while, conversely, net financing materializes lower several years out—a function of further debt management and the group’s interest rate derivatives. Ultimately, it is rare to see such a cash-generative business trading at such multiples, steadfastly and aggressively returning capital, all while being only modestly levered—Imperial sports 1.9x Net Debt/EBITDA and a CoD of ~4.7%.

We can endlessly debate over the specific rate of change over any one operational segment or variable, but the future is bound to throw in a mix of welcomed and unwelcomed surprises alike. The truly silly aspect of all of this is that the above assumes no change in share price. Intuitively, one would expect the market to eventually weigh shares with their earnings—but in Imperial’s case, perpetual dismissal regarding the core business may act as an overhang. That should be welcomed. It is clear, at the rapid pace at which equity is being retired, that a lower share price is capable of having the greatest compounding effect on long-term returns. Conversely, a significant positive rerating would weigh down that exact dynamic; dampening repurchases, slowing the rate of absolute dividend reduction, and to an extent, limiting the group’s flexibility. Returns will be mechanical, and as I’ve said before, this animal feeds on continued pessimism.

If you enjoyed this piece, hit “♡ like” and give it a share.

Questions or thoughts to add? Comment on the site or message me on Twitter.

Ownership Disclaimer

I own positions in Imperial Brands and other tobacco companies such as Altria, Philip Morris International, British American Tobacco, and Scandinavian Tobacco Group.

Disclaimer

This publication’s content is for entertainment and educational purposes only. I am not a licensed investment professional. Nothing produced under the Invariant brand should be thought of as investment advice. Do your own research. All content is subject to interpretation.

Tags: MO 0.00%↑ BTI 0.00%↑ PM 0.00%↑

Thank you for the article Devin! As always I think you have provided a balanced assessment of the company’s results and prospects.

Very little potential upside is priced into the stock. Imperial would likely be a beneficiary if NGPs uptake were to slow down. That’s not anyone’s base case but who knows? In part that will depend on how governments treat NGPs. For instance Denmark just increased taxes on nicotine pouches by $1.70 per pack: https://news.bloombergtax.com/daily-tax-report-international/denmark-raises-tax-on-nicotine-pouches-restricts-alcohol-sales.

A minor question: are you concerned by the working capital build? If memory serves, there was a £300 WC build due to increased inventories. If there’s no such WC build in 2024, Imperial would be in a position to increase their buyback.

BATs has a leading market share of Velo in Sweden and a big share of UK market. USA Velo is a completely different product to BATs superior Europe Velo version and BATs waiting for the FDA approval of EU version, maybe in 2024/2025. USA inferior Velo is just a name change. No information on imperial brands pouch yet apart it ready.