Haypp Group: Rerouting

“The rapid and sustained growth of nicotine pouches is expected to generate increased scrutiny, and, in many cases, the scrutiny is warranted. We will continue to invest significantly into compliance, and we recognize that it is not only a source of sustained competitive advantage, but it is also the right thing to do.” – Gavin O’Dowd, Haypp Group CEO, Q3’24 Call

Haypp’s operations and equity have shown whirlwind performances this year. Early gusts provided the group with swift ascent. My Q2 note sang praise at just shy of the 52w high closing price of SEK 113. It was not long until a cold front of legal and market challenges met the company, driving shares down 45%, essentially to where they were when I first covered the name in February. Your view on whether this is an unresolvable rout or a rational rerouting appears to depend heavily on your horizon.

Two days before Haypp Group released its Q3’24 earnings, I wrote on Substack Notes:

Haypp Group reports Q3'24 soon. Some thoughts:

As mentioned in my Sept. note, I don't find the Swedish snus license issue alarming. Haypp will implement complete PoS + PoD verification, rendering the reason for revocation moot. The appeal process can draw out the process 1-2 years, in which case snus will already be a far smaller piece of the total pie. There may be a slight hiccup in the interim if switching to complete PoS + PoD deprives some rural consumers, but nothing that moves the needle materially when looking out further.

Google's last large algo update began on August 15, and the rollout ended in early September. Unsurprisingly, this caused some SERP volatility amongst Haypp's sites and competitors, moderating into October. While the net result looks favorable for Haypp's portfolio in the aggregate, it will be interesting to see if any impact is noted during remarks.

The California situation is front-and-center. The temporary suspension of state sales obviously drags on Growth Markets, but above all else, how Haypp addresses all stakeholders is paramount. They undoubtedly have comprehensive data, allowing a complete review of their processes. Also, note that Haypp's US sites no longer list shipping from Colorado or New Jersey warehouses, leaving only Texas listed. It is speculative, but this could reflect a change in direction regarding 3PL reliance, either relating directly to the California situation, relying on E-Motions for greater warehouse automation, or both.

Added to the mix of variables affecting the fast-growing US, the ZYN shortage persists despite production capacity improvements. Capped ZYN sales will have pushed more sales into other pouches, driving the average dollar order size further down.

While it will not be reflected in Q3 figures, Haypp's US sites and competitors have routinely shown significant outages of most ZYN SKUs during October and November so far. For Haypp, this likely correlates to running out of stock despite capping sales. A more speculative (and dangerous) view would be that PMI may be less inclined to feed the online channel in the current climate while zyn (dot) com sales remain off and PMI completes its supply chain and market audit to identify bad actors handling illicit volumes (foreign wholesalers, sites selling non-US versions, etc.).

Emerging Markets will be treated as an afterthought—and perhaps rightfully so, given the issues facing Core and Growth Markets. Nonetheless, reinvestment and growth rates of EM, along with any disclosures providing more transparency, will be welcomed.

I look forward to reading the results, hearing management's remarks, and providing my perspective in a future note. No matter how you chop it, Haypp offers excellent insights into how the industry, specifically the NP category, is evolving.

Haypp’s Q3’24 results affirmed that several of these points are far more pressing than others. Let’s dive right into the deep end.

California

In September’s legal update, I opened with the California situation, specifically the San Francisco lawsuit, followed by Haypp’s likely actions in response, and a mix of other essential considerations. To gain fuller context, I recommend revisiting the piece in its entirety.

What we knew at the time was that following the lawsuit’s filing, Haypp quickly shut down all sales to California. This was decisive, unmistakably reflecting the group’s seriousness. I also noted in the piece:

The complaint requests that the court order Northerner Scandinavia to pay the Plaintiffs’ attorneys’ fees and costs, civil penalties for each violation, plus any additional measures that the court deems reasonable. While specific actions were cited, the complaint’s Factual Allegations also state that the total dates and quantities sold will be determined at trial. Despite whatever differences between accounts might exist, considering the time, costs, and uncertainties related to trial, a settlement appears preferable.

Haypp Group has set aside SEK 11m, which is reserved for their current best estimate of the total cost of the above. There is nothing definitive about the actual result—it’s in the group’s interest to resolve it quickly, and the government is surely attempting to extract maximum dollars.

I previously highlighted that the lawsuit concerned the San Francisco Health Code and California’s STAKE Act, not the ‘California Flavor Ban’ SB 793. Now, it is also known that, even if a settlement is reached, sales in California are likely to remain suspended due to uncertainty surrounding new legislation. As I understand it, this relates to Assembly Bill 3218, which appears to encompass online sales and out-of-state sales concretely.

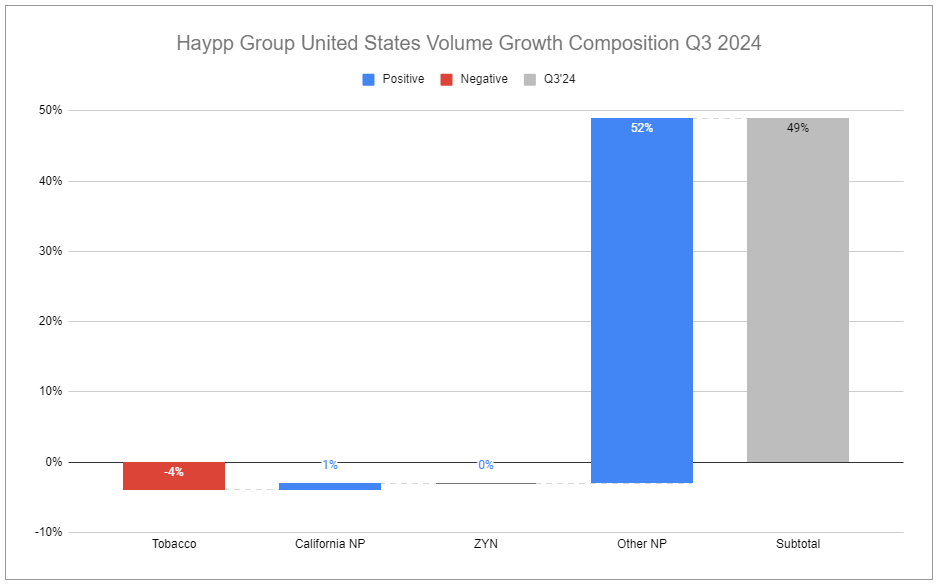

So long as Haypp’s Californian sales are offline, consumers in the state are going to competitors. Should Haypp resume sales and reconnect to previous consumers via email or otherwise, if all that is allowed to be sold are unflavored products, the group’s value proposition will be undeniably diminished. Timing is unknown, but it should be understood that if sales in California resume, Haypp’s associated sales volumes and net revenues will look far different. If I were forced to guess, it would be sometime in Q1’25, with a haircut of more than 85%. Additionally, California represented a large portion of Haypp’s legacy oral tobacco sales, although those sales are a smaller part of the group’s total, which I touched on in Q2:

Access to the largest segment market by far, the United States, was provided with the acquisition of Northerner, whose portfolio of sites had previously placed greater emphasis on legacy oral tobacco brands. While Haypp prioritizes nicotine pouches, legacy products still make up a non-zero portion of volumes. Of the company’s top 10,000 ranked Google keywords, a number of top rankings are for varieties of Copenhagen, Skoal, Stokers, Red Man, General Snus, Grizzly, and so on.

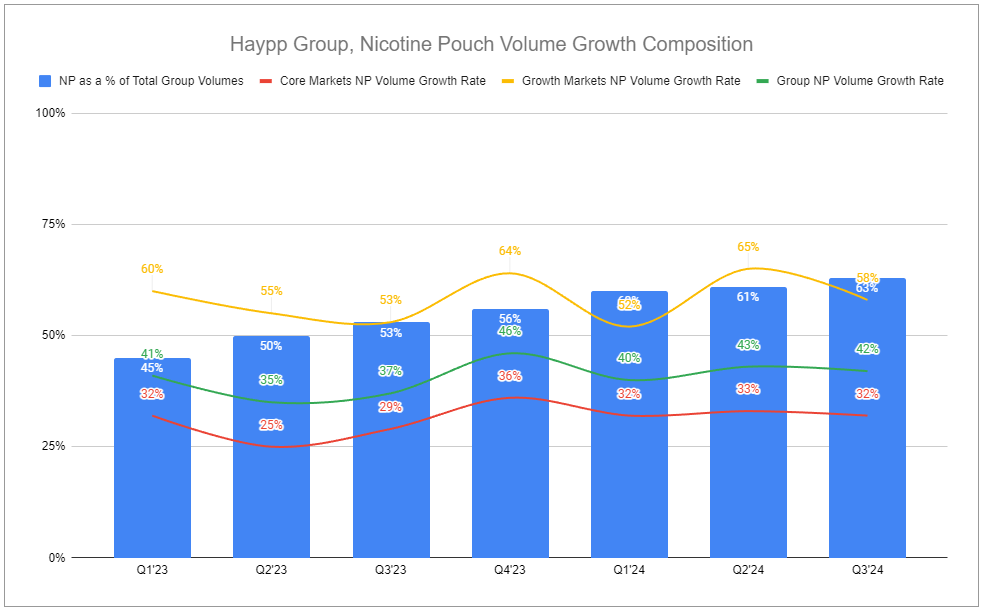

Many of the group’s legacy oral tobacco products are flavored variants. Since a large portion of those sales were being made in California, and since only non-flavored variants will be permitted there in the future, Haypp is winding down its legacy oral tobacco sales at the end of Q4’24. Haypp’s nicotine pouch sales in California represent approximately 2% of total group volumes. Legacy oral tobacco in the United States is about 1% of total group volumes. The United States represents roughly 1/5 of the group’s total volumes, so nicotine pouch sales in California make up roughly 10% of United States volumes, and legacy oral tobacco makes up 5%.

The idea of the group’s volumes dropping by 15% in one of its largest and fastest-growing markets sounds alarming. It isn’t pretty. However, several points suggest the actual financial impact will not be quite as severe as implied. Haypp’s NP volumes in California haven’t been growing like across the rest of the country as of late, following the trend reversal after the initial bump from the state-level flavor ban. California has a high state-level excise rate, which certainly has not aided growth either. These sales have historically been lower margin compared to other states due to shipping constraints. In addition, the profitability of Haypp’s legacy oral tobacco business has been minimal, and it’s always been an afterthought—completely non-essential to the group’s longer-term strategy. These legacy oral volumes have been rapidly shrinking. The company was already planning to wind down the legacy business in 2025, so the push forward to Q4’24 isn’t anything extraordinary.

I’d assume that Haypp is directly marketing via email to its verified adult consumers of legacy oral products, aiming to incentivize trialing and switching to nicotine pouches as the legacy business is wound down. Although Haypp has never invested meaningful resources in the legacy oral tobacco business in the United States, winding it down has one distinct benefit. Those categories comprise a substantial portion of the main navigation on the Northerner website. Optimizing the UI strictly for pouches can improve UX pathways and, ultimately, conversions. There is also the potential that the group condenses all legacy categories within the navigation, temporarily retaining all related category and SKU pages and repurposing them to steer consumers toward pouches, benefiting from lingering SEO rankings until completely cutting it. Either way, trading prime website ‘real estate’ that currently serves a quickly-shrinking, lower-margin business, half of which is located in a state where sales are suspended, and dedicating it to what is going to move the needle over the long term absolutely makes sense.

As far as sales in California and of legacy oral tobacco products go, I would assume most people are fixated on the volumes, regardless of profitability or growth. I still find the chief concerns to be elsewhere. In September, my take was clearly stated:

You could estimate California’s contribution up until the moment sales were suspended. Then, there’s some guesswork on whether or when sales will resume. After that, there are all kinds of questions. What’s the impact of selling a reduced SKU set? How many prior customers convert back? The fuzziness of it all points to time being better spent thinking about a more critical matter. Credibility. Compliance, specifically age verification, is at the heart of the Haypp Group thesis. How the group demonstrates its commitment to consumers, suppliers, regulators, and shareholders is paramount, and I look forward to seeing how they address the California situation.

The initial decision to sell flavored products to adult consumers in San Francisco was predicated on the legal opinion provided by an external law firm. There is little doubt that Haypp will be sinking more into legal resources to navigate changes in existing and new markets. The internal measures the group takes to ensure all sales and distribution processes are not just compliant but industry-leading are integral to the group’s image. The SEK 11m, at the end of the day, is affordable. It is the cost to Haypp’s reputation that is worrying. I recognize that due to the San Francisco suit being unresolved, the group is in a difficult position. Nonetheless, these points are deserving of greater communication.

United States infrastructure

I previously noted some subtle changes over time to the shipping information on Haypp’s United States websites.

This is the result of Haypp ending its 3PL relationships and consolidating shipping to its owned Texas warehouse. It was planned far before the issues in California. While most of the Q3’24 elevated reinvestment rate went into Emerging Markets, a portion was related to this. The warehouse in Texas was already set on a long-term lease and is large enough to absorb all volume previously handled by 3PL, plus anticipated growth. It is currently being outfitted with the same automation systems that are used in the Core Markets, which are provided by E-motions.

One major advantage of automating this warehouse is that order processing and fulfillment can occur faster, so there is no real detriment to getting products to the doors of adult consumers even though the warehouse is located farther away from many. An even more significant advantage is that automation drastically reduces the pick and pack costs associated with each order. In Sweden, automation has driven those costs roughly 70% lower than in the non-automated United States. This will not be immediately evident in the financials, as the impact occurs with scaling units. Over time, I would expect it to be meaningful.

Significant US ZYN outages online

Haypp’s Q3’24 report disclosed that, at the end of the quarter, the company had difficulties sourcing ZYN in the United States and that, should such difficulties continue, the group’s sales of the product in the United States would become negligible in Q4’24. This is roughly 35% of the group’s United States sales, ex-California. Quite problematic. A basic timeline helps set the stage, so let’s start there. When I published my initial writeup on Haypp Group, one of the listed risk sets was as follows (emphasis added):

One looming risk that is difficult to quantify is the continued evolution of next-gen nicotine products and how consumers will behave in terms of trial, adoption, preference, poly-usage, and usage frequency. Continued innovation within the nicotine pouch category is a definite tailwind for Haypp. But there is no guarantee it will navigate potential new other categories equally well. It may very well underinvest in underestimated opportunities and overinvest in others that fall short. Likewise, the rapid growth of the nicotine pouch category has led to manufacturers needing to continually reinvest in production capability. Haypp’s success is tied to this, and the company must maintain strong relationships with those parties.

This risk set was swiftly demonstrated when Philip Morris International reached maximum production capacity for ZYN in the United States earlier in the year as demand accelerated, leading to widespread shortages. I’ve tracked developments closely in published notes on PMI. In the Q1 PMI note, despite murmurs of developing shortages, PMI’s ZYN figures provided a signal for strong Haypp results. In the Q2 PMI note, I argued:

Across most potential futures, considering the evolving competitive scape, regulatory dynamics, enforcement, and current changes in volume share courtesy of ZYN capacity constraints, a potential major benefactor is online distributor Haypp Group.

When the ZYN shortages began, it drove consumers online at an accelerated rate, benefiting Haypp. Haypp began to limit ZYN orders monthly for consumers. Further delaying visibility into the company facing the issue was a factor I touched on in my initial writeup:

There was a substantial increase in inventories in Q4’23, but this was completely elective, designed to take advantage of anticipated inbound price increases for specific products in early 2024.

Much of this excess inventory was ZYN in the United States, which did experience a price increase of $0.15 per can in Q1. Yet, another development was brewing in tandem. During PMI’s Q2 call Q&A, management was asked about illicit volumes entering the United States. Emmanuel Babeau, PMI CFO, did not offer much detail, and I then wrote:

There are a few direct ways to interpret the above exchange. The scary interpretation is that an illicit pouch market is rapidly growing, and because illicit volumes are sold through untracked channels, PMI has limited data on the extent to which this is occurring. The far less problematic interpretation is that, as Emmanuel Babeau stated, there is nothing occurring to a material extent, and therefore, there is no material data being produced. I lean towards the latter explanation for several reasons. Firstly, if PMI’s Scandinavian variant was entering the US unlawfully to a material extent, the company would indeed have data showing a divergence between shipment volumes across geographies and retail offtake over time. Secondly, while there are brick-and-mortar retailers selling illicit products, the majority appear linked to a number of online retailers, many of which received warning letters earlier in the year.

I concede that, while it may have been true then, I underestimated the future effects a continued ZYN shortage would have on foreign sites illegally selling European pouch variants into the United States, as well as occurrences of foreign wholesalers getting products to various physical retail outlets. As things progressed, it appeared that the environment would become more difficult, and I stated in the Q3 PMI note:

Despite incremental supply improvements within the broad US market, online channels, such as Haypp’s US sites, have recently shown worse ZYN outages. Sales on PMI’s zyn (dot) com remain turned off. Then there is the question of the many players moving foreign products into the US unlawfully. While PMI specifically stressed its efforts to tackle illicit volumes in the US, I can confirm that many sites still eagerly sell such products to US customers.

The exact rate of change on the US front is unknown, but change it will. PMI will undoubtedly resolve many of the issues faced, one way or another, perhaps to the detriment of others.

One concern has been concentration risk—ZYN accounts for a large part of Haypp’s US sales. If you hypothesize that ZYN is integral to Haypp’s competitive position in the United States, the current real-world setup is probably a better test than anything you could dream up in a lab.

Considering the moving parts, they all ultimately tie into the ZYN capacity issues. Shortages accelerated the online channel, which accelerated illicit sales from foreign sites and wholesalers, which accelerated concern that pouches could get wrapped up into a giant legal mess, which appears to have led PMI to take conservative measures in response to assess its supply chain and the market, primarily tackling non-compliant foreign actors. Those foreign non-compliant sites are still selling into the United States (including to me) despite previous FDA warning letters. However, several have disallowed me from ordering European versions of ZYN, stating, “We can’t ship these specific SKUs to your destination.” I lean to believe that PMI is attempting to squash those sales directly. Further, if you check communities, such as the nicotine pouch subreddit, you will see many posts and comments from the past few weeks about overseas shipments becoming stuck in customs more frequently and for extended periods. Although many of these shipments will be released eventually and head to the purchasers, government agencies taking logs are likely setting up for future rounds of enforcement actions.

While Haypp Group holds roughly 85% of the legal online market in the United States, previous estimates put that share at 55% when accounting for foreign illicit sites. This issue has likely grown worse in the last half year. There’s no timeline, but if the illicit issues are largely tackled, there are several clear implications. The first is that the online market shifts more in Haypp’s favor. Second, PMI is incrementally improving ZYN production capacity throughout the remainder of this year and next, so shortages across the board should be alleviated despite the growing total demand.

Those hypotheticals may be wishful, and even if they occur, the vast extent will not be in the remaining half of Q4’24. If you add Haypp’s ZYN volumes to its pouch volumes in California and legacy oral tobacco volumes, they total about 45% of United States volumes in Q3’24. The mere suggestion that the group’s United States volumes could drop so significantly in Q4’24 is alarming. But just like California and legacy oral tobacco, the actual impacts of ZYN’s absence aren’t entirely straightforward.

The spike in online channel adoption resulted in Haypp’s traffic from organic search increasing by 101% y/y in the United States in Q2’24. Despite having ZYN available, sales per consumer were capped, driving sales of non-ZYN pouch brands up by 121% y/y. But there were several caveats. If the ZYN shortage drove this, any improvement in availability within physical retail channels could unwind it. ZYN rationing and non-ZYN sales drove down the average dollar order size. At the time, Haypp admitted there was uncertainty regarding the retention rates of these new consumer cohorts. Although PMI is increasing capacity, and the physical retail channel is improving ZYN availability, in Q3’24, Haypp’s non-ZYN pouch sales in the United States increased by 130% y/y, excluding California. It appears that retention is pretty robust.

The real questions are: To what extent do Haypp’s non-ZYN pouch sales continue, and does the company manage to retain the majority of active consumers? The only way that would-be ZYN sales would result in 0 in Q4’24 would be if there were no alternative products. But there are alternatives.

You can walk through this intuitively. Presently, if an adult consumer lands on one of Haypp’s two United States sites, ZYN is still well-displayed. If that user selects the ZYN category, all SKUs are out of stock, with a ‘Show Similar’ button that paths to other brands with a similar flavor and strength profile. If they instead click on the SKU directly, all of the SKU data will still be available, but a popup alert will reiterate out-of-stock and suggest looking at alternatives. Scrolling down shows other pouches as well. There is no doubt that this is driving a significant portion of users to branch out into other brands, many for the first time.

The experience and satisfaction a user has with alternative products play a defining role in retention. If all that was available were low-grade products, retention would be dismal. Fortunately, there are some very good products with an appeal that should be readily understood but probably isn’t. Sesh and Lucy both stand out in feel and also have flavors that ZYN doesn’t have. FRE appeals to higher-strength users, with strengths exceeding all ZYN SKUs. And then there is zone, which I’ve noted several times and recently claimed (emphasis added):

Imperial Brand’s new horse, zone, is already running. Although sales data is more limited in history, zone is a much better product than I believe most are ready to give credit—quality packaging, incredibly soft pouches, long-lasting flavor, and strength and flavor assortments that closely overlap ZYN point to a product capable of winning many over in a blind test.

These mentioned products do not have the same distribution or physical retail relationships that make ZYN widely accessible offline, although they are growing. I see it as inevitable that awareness of brands such as these will continue to increase. Beyond product qualities, price is a critical consideration for trial and retention. Many of the MSRPs of these products are within similar ranges of ZYN, but Haypp’s retail prices are significantly lower than ZYN’s retail price range, presently varying ~20% less for Sesh and ~45% less for zone.

Mix shift

But wait, you say! At much lower prices, this should materially reduce average dollar order size and Haypp’s net revenues from associated sales. This is correct but does not have wholly negative implications. ZYN is the most well-known brand in the United States. It is priced at a premium. To spur consumer trial and repeat purchases, other brands undercut ZYN and sport a lower retail price. However, other brands also carry lower list prices at wholesale. The differential between wholesale and retail prices of these products is wider than that of ZYN. Therefore, despite retail prices being meaningfully discounted, other brands typically carry more favorable unit economics for Haypp.

Incoming

Velo+ is coming soon. I still have not accessed the product, and while I am cautious anytime BAT makes claims about new products, I have heard from others that this is a noteworthy product. Much like the pouches introduced into the United States market this year, an initial route-to-market will likely be on Haypp sites. There is no clear timeline on when the FDA finishes the PMTA backlog, in which many ‘2.0’ pouch versions are stuck waiting, but even in the interim, other brands, technically marketed and PMTA-filed before earlier deadlines, could be introduced to the online channel. One way or another, competitive brands are coming. This will drive Haypp’s media and insights business, and it will surely test ZYN’s position in the marketplace.

Growth Markets

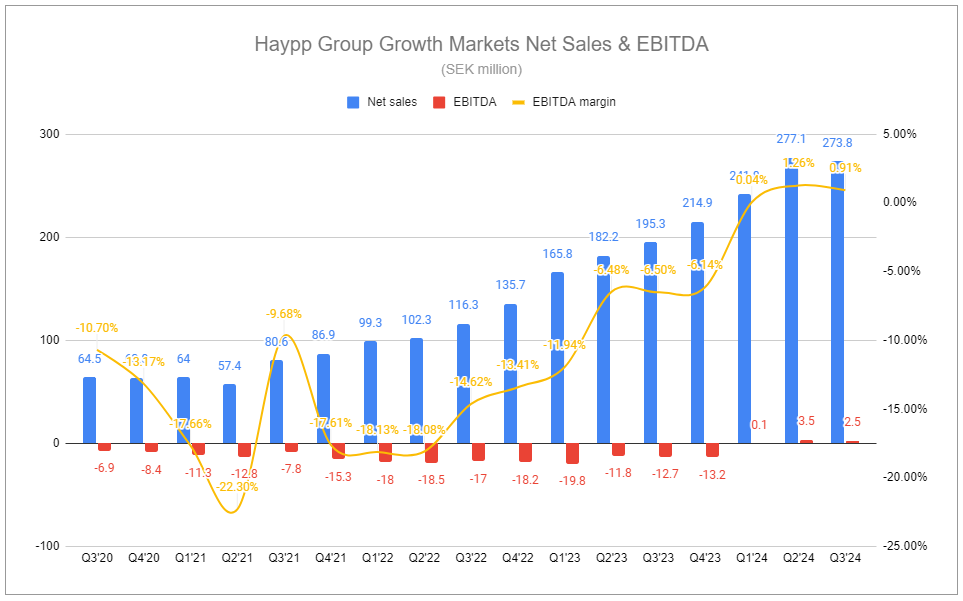

The United States is the most significant country in the Growth Markets segment, but it is not the entirety of the segment. Other Growth Market countries have kept their growth trajectories intact. While Q3’24 net revenues for the segment were down sequentially and are bound to take a hit in Q4 and likely Q1’25, the long-term prospects remain intact.

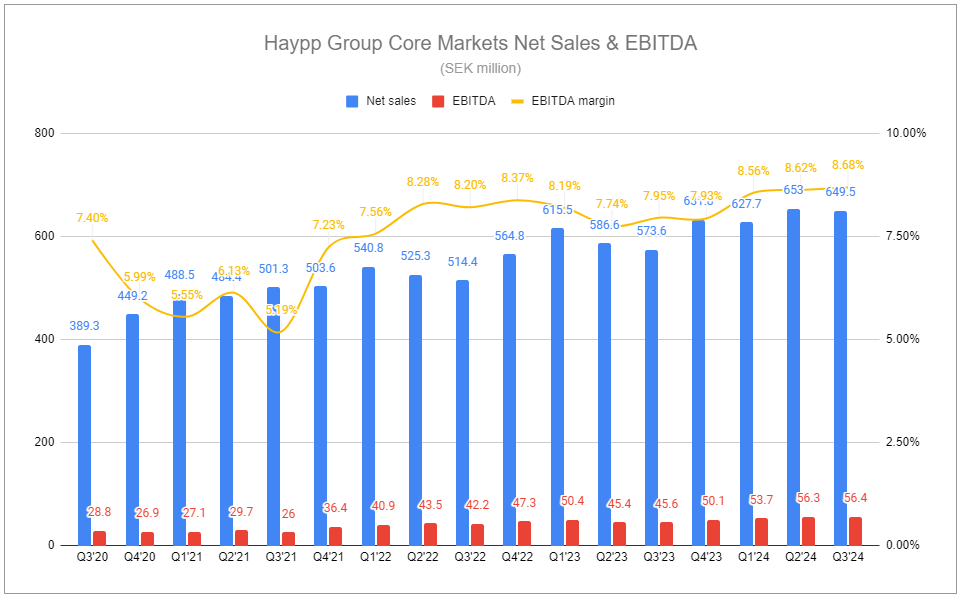

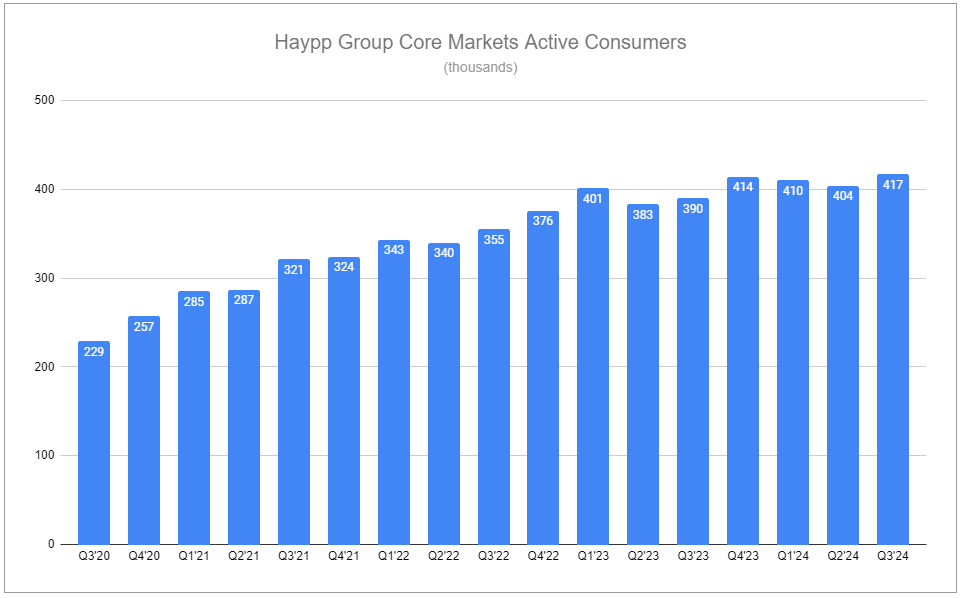

Core Markets

Concerning its Swedish tobacco product license, Haypp management confirmed many of the points in my September legal update. The appeal process will likely take 1-2 years, during which it would be ‘business as usual.’ A favorable outcome from the appeal process is likely. One, the decision to revoke the license was not unanimous, with two of the five committee members dissenting. Two, the issue concerns demanding the use of PoD age verification over PoS for snus. Haypp has implemented PoD verification, rendering the original rationale for the revocation moot. It is now up to the courts to decide. Also, consider that since snus sales are quickly declining in Sweden while nicotine pouches grow, even if a negative outcome is reached, the net financial impact should be far less than what the current headline numbers suggest. Not to mention, this does not concern nicotine pouches, which are regulated by a separate body in Sweden, and nicotine pouches are more profitable than snus for Haypp.

While the Swedish snus license remains in limbo, Haypp Group highlighted the changes in Sweden’s policy goals. I mentioned this development in September, stating:

The changes are subtle initially, but as you complete the page, the proposal’s significance becomes unmistakable. Sweden, the country that birthed snus and now nicotine pouches, leading to a remarkable drop in heart disease and lung cancer, remains firmly on the edge of progressive policy. Instead of focusing on reducing tobacco use, the proposed new target is to focus on reducing medical and social harm. The proposal separates tobacco and nicotine, highlighting the risk continuum across product categories. That risk continuum already influences how these products are taxed, and the proposal firmly extends the concept’s application. Sensible, holistic Tobacco Harm Reduction.

This policy proposal proves deeply beneficial for Haypp’s nicotine pouch sales in Sweden.

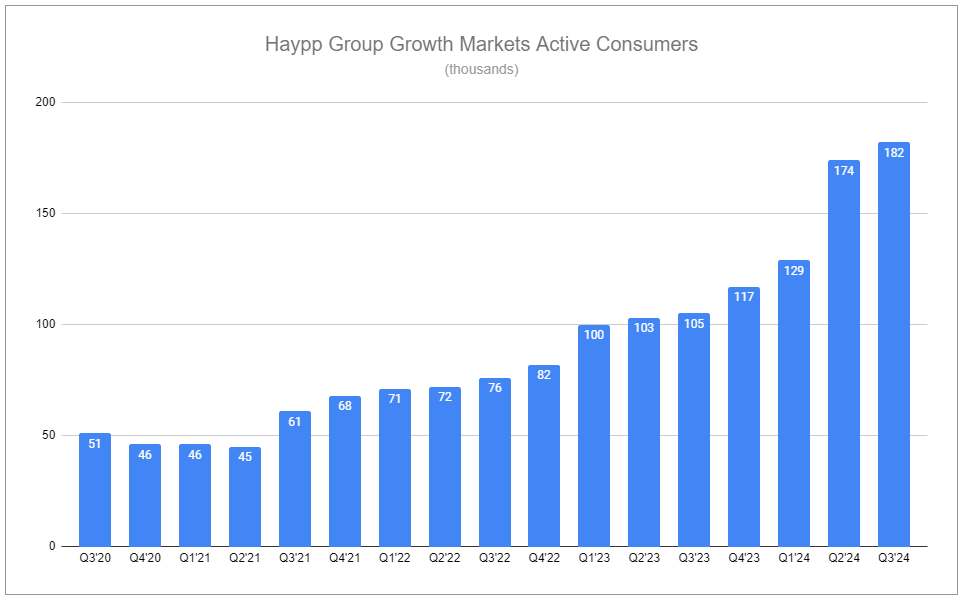

For Q3’24, Growth Markets’ net sales increased by 13%. Nicotine pouch volumes grew by 32%, with the snus decline rate sustaining as a headwind. Active consumers increased by 7% y/y, and EBITDA margin expanded by 0.7pp, driving an EBITDA increase of 24%.

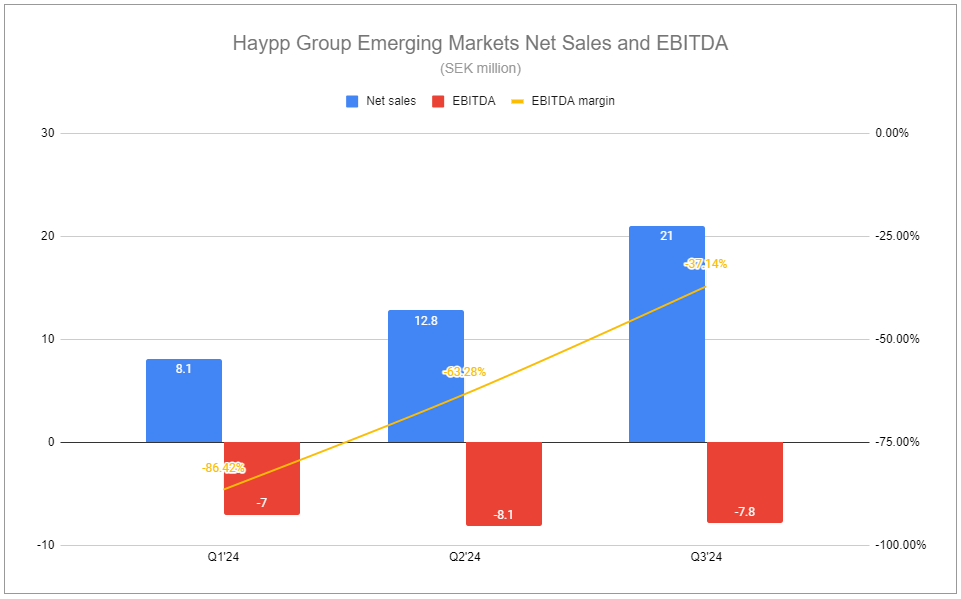

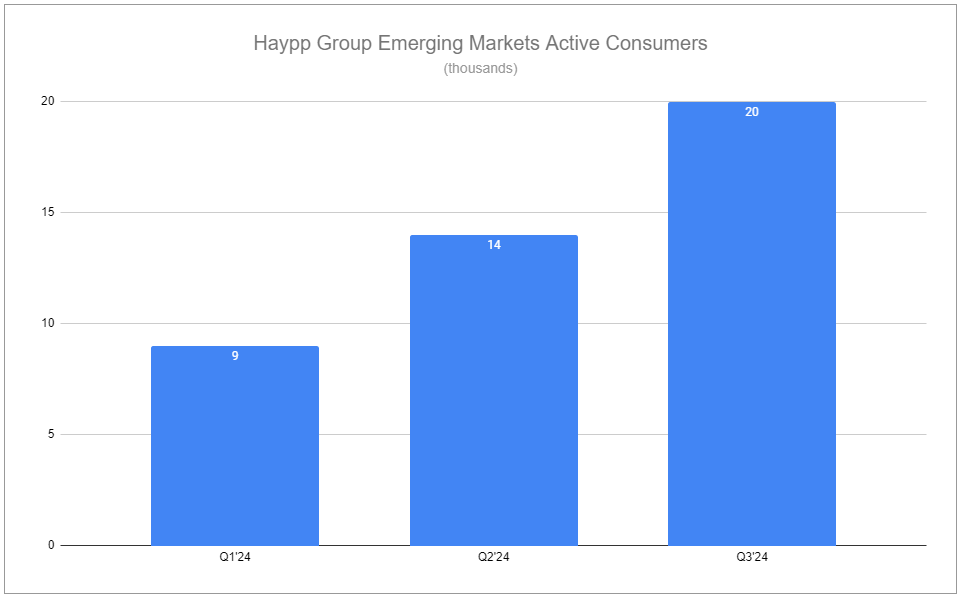

Emerging Markets

Emerging Markets grew net sales by 64% sequentially, grew active customers by 42%, and continued to sport an expected loss as the group continued to reinvest and grow the subscale business—this is where the majority of the quarter’s elevated reinvestment rate went. Encompassing vaping products, floating concerns exist that the United Kingdom’s interest in banning disposable products would weigh down Haypp’s nascent endeavors. Such a ban will inevitably further foster the illicit market. However, for adult consumers interested in convenience and affordability, Haypp’s inclusion of pod-based vaping is promising. While the devices aren’t inherently attractive for retail purposes, the pods are. Pods are smaller, lighter in weight, and have higher margins than disposables. Likewise, over the last few weeks, Haypp’s Emerging sites have begun to offer heated tobacco units, as well as non-tobacco nicotine-infused units for heat-not-burn devices. Like pods, these offer incredibly attractive unit economics.

SEO

My curiosity surrounding Google’s last major search update, which occurred in August, still remains. However, there is no concern. The rankings of Haypp’s portfolio of websites continue to sport favorable ranking profiles following the initial episode of SERP volatility.

Rerouting and the broader view

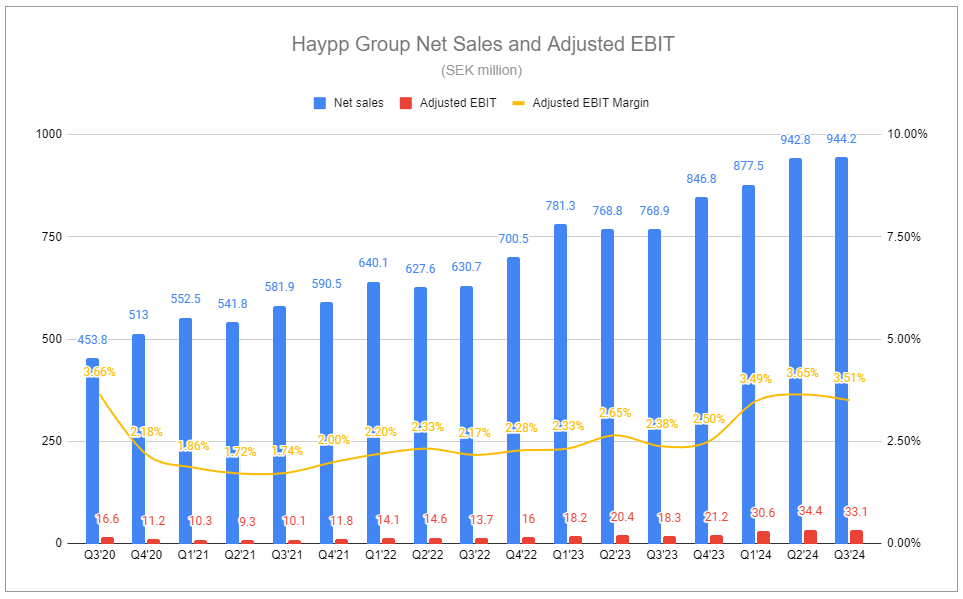

There is no escaping it. Q4’24 will be a weak quarter, and Haypp’s challenges have forced a partial rerouting. There is virtually no chance the company will reach its 2025 net sales goal of SEK 5 billion. The abrupt removal of volumes in the United States will diminish operating leverage in Growth Markets. However, when taking the broader view, plenty can go right.

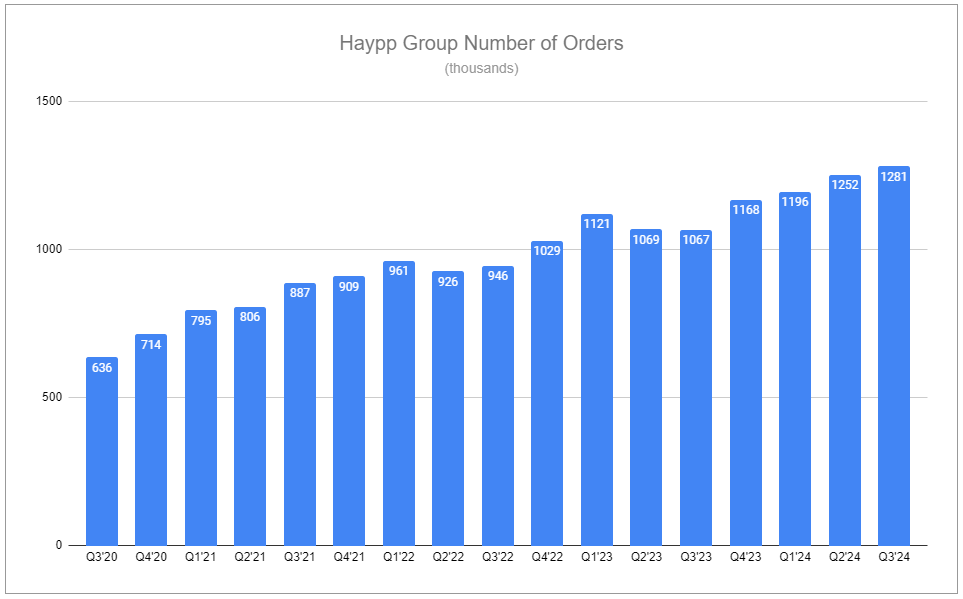

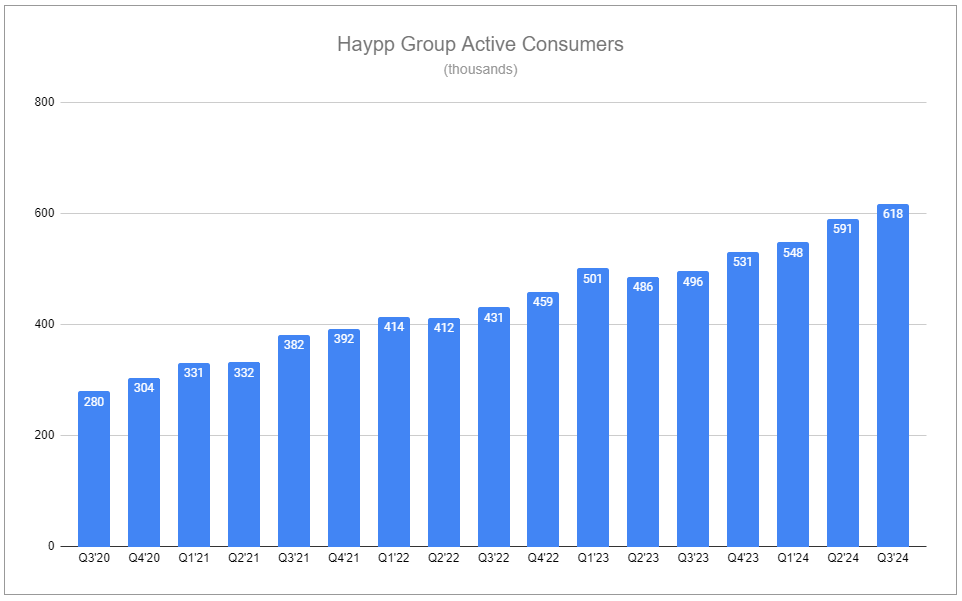

In short order, we will see the effects of a temporarily ZYN-less Haypp in the United States and how well other brands supplement would-be sales. Beyond the financial impacts of cutting the less profitable legacy business, the story and focus will be simplified. Haypp sits under 11x EV/EBITDA and just over 9x EV/Core EBITDA. The challenges facing the United States market are the focal point, but the strengths in Emerging and Core can’t be overlooked. The Swedish license hangup is more likely than not to be favorably resolved, and the NP category’s demand is stronger than ever; Haypp’s active consumers and orders are climbing higher still, and there is a clear potential for the online channel to grow and improve.

Just as the 2025 net sales goal will be missed, margins will struggle, too. However, physical and digital infrastructure, improved mix shift, and scale recovery from NP volume growth still provide room for large improvement, along with the benefit of media and insights. The initial 2025 goals were provided in 2021. Next quarter we can expect a thorough articulation of all of these considerations and a new multi-year outlook. **Haypp’s Q3’24 report states an update on medium-term targets will be provided in ‘Spring 2025.’**

Thanks for reading. Enjoy this piece? Hit “♡ like” on the site and share it.

Questions or thoughts to add? Comment on the site or message me on Twitter.

Ownership Disclaimer

I own positions in Haypp Group, as well as positions in tobacco companies such as Altria, Philip Morris International, British American Tobacco, Scandinavian Tobacco Group, and Imperial Brands.

Disclaimer

This publication’s content is for entertainment and educational purposes only. I am not a licensed investment professional. Nothing produced under the Invariant brand should be thought of as investment advice. Do your own research. All content is subject to interpretation.

Devin, thank you this is very helpful.

The main concern I have is the alleged violations of the STAKE Act in CA. The worst case interpretation is that Haypp has flagrantly violated multiple requirements of the STAKE Act, including (1) the need to match ID address with credit card address (2) signatures at PoD (3) specific labelling requirements (4) phone calls required after 5pm to confirm orders. Haypp hasn't substantively commented on the alleged STAKE Act violations, and perhaps that's the appropriate thing to do, and I'm sure that's what their lawyers advised. So we don't have a good sense for the validity of the allegations. However, in reading some of the tea leaves my spidey sense is tingling. For example:

- Haypp has given quite good information on the Stockholm legal situation, and as it relates to the San Francisco complaint regarding the flavored products Haypp has also given helpful color. They mentioned that they had advice from a reputable law firm that they were able to sell flavored products in SF, so they have effectively admitted the allegations in that instance but explained to the market that they feel that they acted reasonably. However they have said nothing on the alleged STAKE Act violations - which is a different posture to the SF flavored product allegations in particular.

- they have stopped all sales to CA. They say this is because of pending legislation, but the legislation is pending (why can't you continue selling until the legislation is passed?) and the legislation is only related to flavored products (why can't you continue to sell non-flavored products in CA?). Is it possible they are banning CA because they don't have the systems in place to comply with the STAKE Act?

The biggest possible downside here is that Haypp just hasn't been compliant in many jurisdictions beyond CA, and CA is the canary in the coal mine. And that would obviously be a massive issue.

I'm not saying that's a likely outcome, and I'm not trying to be alarmist, but it's hard for me to completely rule out that possibility given the fact pattern.

I'd love to hear your take on the above, including any holes in my facts or logic.

Devin, what’s your view on the likelihood of an EU wide ban on pouches (excl Scandinavia) and how material would that be to Haypp? Poland/Germany/France/Netherlands/Belgium so far seem to driving in that direction.